Welcome to our deep dive into “The Psychology of Money” by Morgan Housel, a treasure trove of insights that transcend traditional financial advice. In this blog post, we’ll explore key takeaways from Housel’s acclaimed book, offering a unique perspective on managing your finances with wisdom and understanding.

1. Savings as Freedom and Security

Morgan Housel sheds light on the real value of savings – it’s less about hoarding wealth and more about the freedom and security it brings. By saving, you gain the flexibility to make choices and the resilience to bounce back from life’s unexpected turns.

2. Wealth is What You Don’t See

Contrary to popular belief, true wealth isn’t about flaunting luxury; it’s about the unseen – the unspent money, the investments growing quietly, and the properties not burdened by debt. Wealth is about the assets you accumulate, not just the income you earn.

3. The Role of Luck and Risk

Acknowledging the roles of luck and risk in our financial journey is crucial. Housel’s perspective encourages us to view our successes and failures through a lens of humility and understanding, recognizing the unpredictable nature of life and markets.

4. Less Ego, More Wealth

The pursuit of wealth should not be driven by ego. Housel advises against taking unnecessary financial risks for the sake of appearances, advocating for decisions that align with your personal financial goals and circumstances.

5. Long-Term Thinking in Investments

Patience and a long-term outlook are key in investment strategies. Housel encourages readers to focus on the bigger picture, looking beyond short-term market fluctuations to the potential for long-term growth.

6. Personalized Financial Strategies

There’s no universal strategy for financial success. Personal finance is deeply individual, and Housel emphasizes the importance of tailoring your financial plan to your unique goals, circumstances, and risk tolerance.

7. The Importance of Being Reasonable

Being reasonable with your finances, according to Housel, sometimes trumps being overly rational. It’s about finding a balance that works for you, especially when it comes to investment decisions.

8. Control What You Can

Finally, focus on what you can control – your savings rate, your expenses, and your retirement plans. Stressing over unpredictable market trends or economic forecasts is less productive than focusing on your personal financial habits.

Conclusion: “The Psychology of Money” offers a fresh perspective on personal finance, intertwining psychological insights with practical financial advice. By understanding our relationship with money, we can make smarter decisions that align with our long-term goals and values. Dive into Morgan Housel’s world of financial wisdom and reshape your approach to money management today.

Hey there, future financial maestros! Are you ready to dive into the world of smart money management? Today, we’re not just talking about saving pennies; we’re exploring how to manage your money like the wealthy. This skill is crucial for anyone aiming to achieve financial independence and is often overlooked in our education. Let’s unravel the secrets to handling your finances with wisdom and foresight.

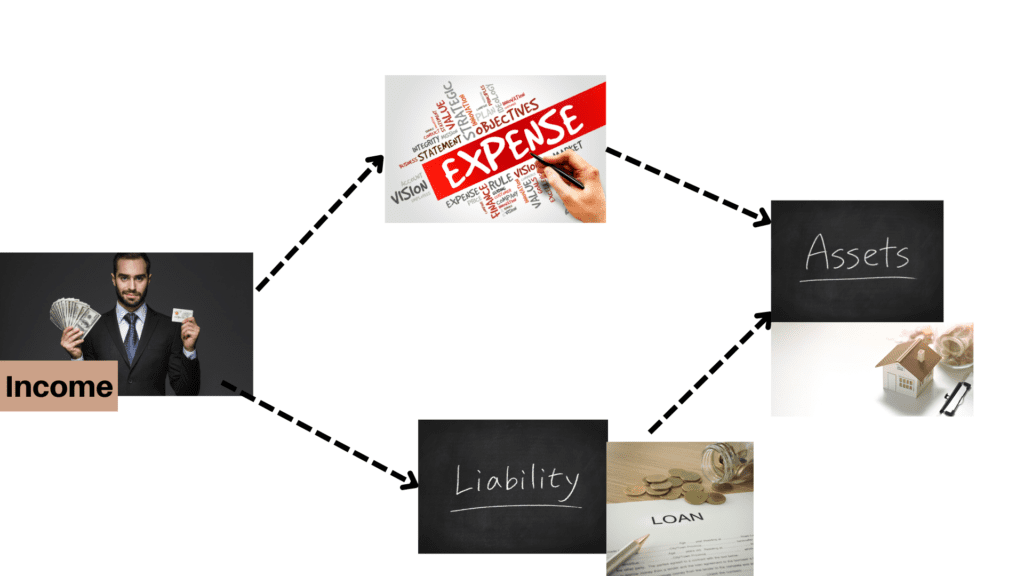

The old Middle-Class Way of Money Management

In the typical middle-class money management scenario, most people earn income and immediately spend it on goods, services, and liabilities like credit card debts and home loans. There’s often a pattern of investing in assets with whatever little is left after expenses. This approach, unfortunately, hampers the growth of wealth-building assets and keeps many in a financial rut.

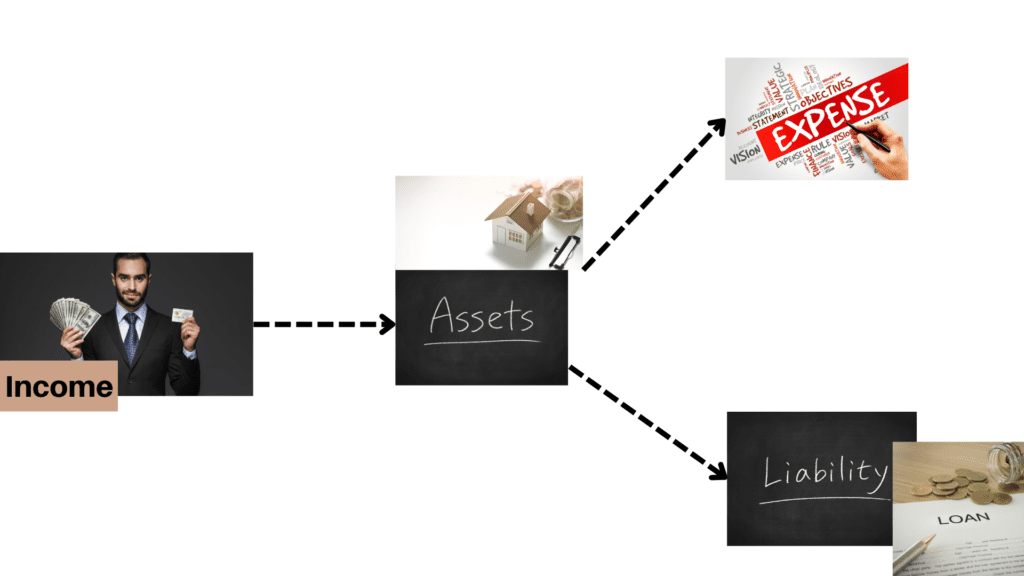

So, how do the wealthy do it differently? It’s all about priorities:

Prioritize Asset Accumulation: When income rolls in, the wealthy focus first on buying assets. This could be stocks, real estate, or any avenue that promises growth.

Manage Expenses and Liabilities: After securing assets, they then manage their expenses and liabilities, often minimizing unnecessary expenditures.

Reinvesting Asset Gains: The golden rule here is to reinvest the returns from these assets into buying more, steering clear of the trap of increasing expenses with rising income.

Robert Kiyosaki’s Concept

The concept of “Pay Yourself First” is one of the cornerstone principles in Robert Kiyosaki’s “Rich Dad Poor Dad.” This idea challenges traditional personal finance advice and focuses on a key aspect of wealth building. Here’s a deeper look into what it means:

The Basic Premise

Traditional Approach: Usually, when people receive their income, they first pay their bills and expenses and then save whatever is left. This approach often leads to little or no savings, as expenses tend to expand to consume the available income.

Pay Yourself First: In contrast, the “Pay Yourself First” method advocates for setting aside a portion of your income for savings or investment before paying your bills and other expenses. It’s essentially treating your savings and investment accounts as the most important ‘bills’ you pay each month.

The Underlying Philosophy

Financial Discipline: This strategy requires discipline and a strong commitment to your financial goals. It’s about prioritizing long-term financial health over immediate spending.

Forced Savings and Investment: By saving or investing first, you’re effectively forcing yourself to save and potentially grow your wealth, rather than leaving saving as an afterthought.

Practical Implementation

Budgeting: Determine a realistic percentage or amount of your income that you can save or invest each month. This should be done after considering your basic needs but before any discretionary spending.

Automated Savings: Automating this process can be highly effective. Set up automatic transfers to a savings account or investment portfolio right when your paycheck arrives.

The Long-Term Impact

Wealth Building: Over time, this practice can lead to significant accumulation of savings and investments, contributing to wealth building.

Financial Discipline: It also instills a habit of living within or below your means, which is crucial for long-term financial stability.

Criticisms and Considerations

Real-Life Challenges: Critics point out that for many people, especially those with low incomes, paying themselves first might not be feasible due to tight budgets and necessary expenses.

Flexible Approach: It’s important to adapt this principle to individual circumstances. For some, it might mean saving a small percentage initially and gradually increasing it.

The Path to Financial Freedom

The ultimate goal? Building a solid asset column. The dream is to have your assets eventually generate enough income to cover your expenses. This means investing more in assets and cutting down on non-essential spending. It’s about setting yourself on the path to financial freedom, where your assets work for you, not the other way around.

Conclusion

Mastering wealth isn’t just about saving or investing; it’s about restructuring your financial priorities to build a sustainable and prosperous future. Remember, managing money is a journey, not a destination. Be patient with yourself and celebrate the small victories along the way. With these strategies in hand, you’re well on your way to becoming a money management pro. Here’s to a brighter, more secure financial future!

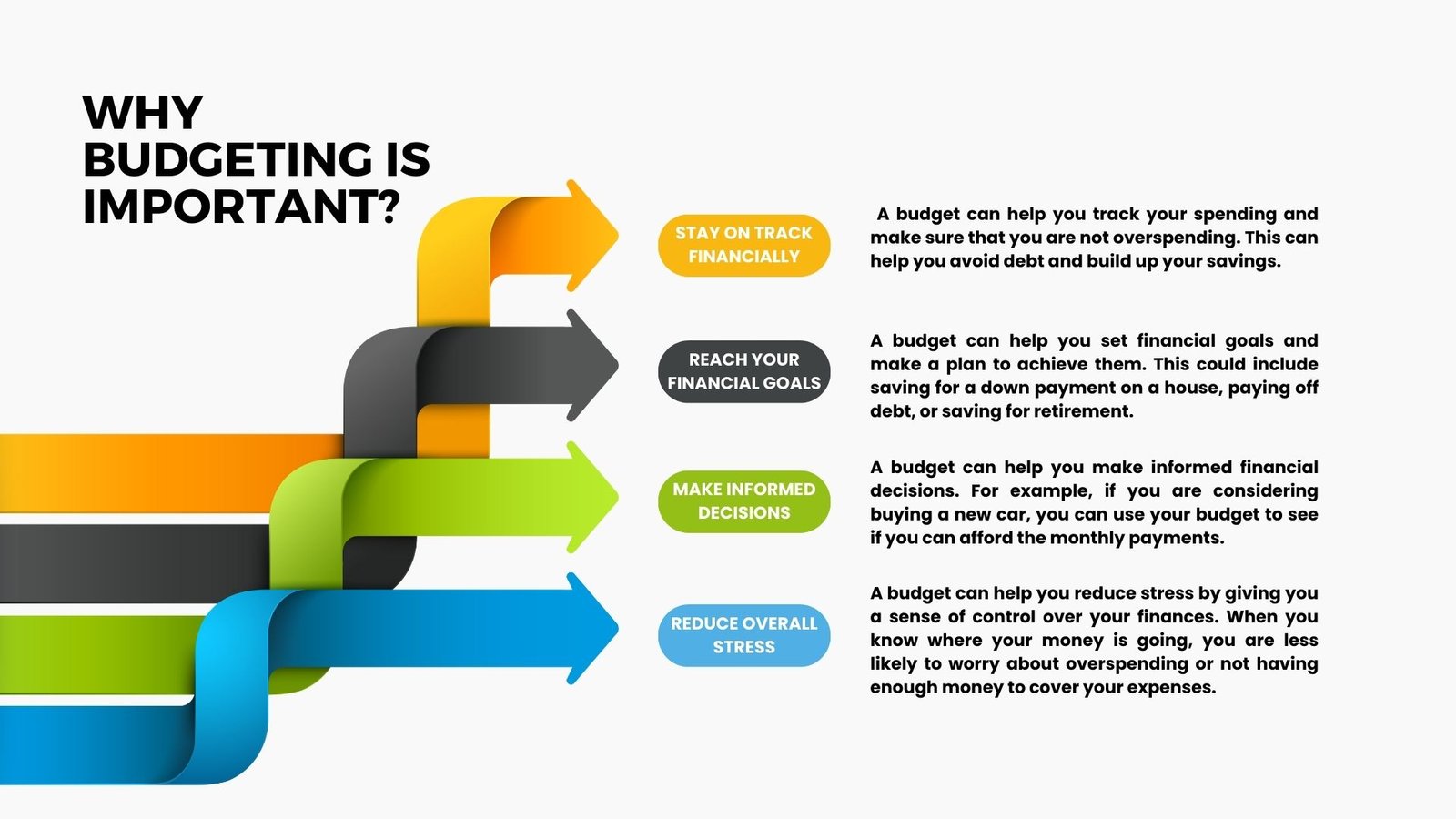

Budgeting is one of the most important financial tools you can use to achieve your financial goals. A budget helps you track your income and expenses, so you can see where your money is going and make sure you’re not overspending. It also helps you set financial goals and track your progress towards them.

However, To make sure your budget is still working for you, it is very important to review and adjust your budget in regular intervels of time. This is because your income and expenses can change over time, and you may need to make adjustments to your budget to reflect these changes. The purpose of this blog post is to provide insights on how frequently you should review and adjust your budget for successful money Security?

Why Reviewing and Adjusting your budget is so important:

1. To ensure that your budget is still realistic and achievable. As your income and expenses change, your budget may no longer be realistic or achievable. By reviewing your budget regularly, you can make sure it’s still working for you.

2. To track your progress towards your financial goals. This will help you stay motivated and on track.

3. To identify areas where you can save money. This could mean cutting back on unnecessary expenses or finding ways to reduce your spending.

Understanding the Dynamic Nature of Budgeting

Budgeting is not a static process. It needs to evolve with changing circumstances. Life events, income changes, and financial goals can all impact the effectiveness of a budget. That’s why it’s important to be flexible and adaptable when it comes to budgeting.

1. Life events: Life events can have a significant impact on your budget. For example, if you have a child, you’ll need to factor in the cost of childcare. If you get married, you’ll need to combine your finances and create a new budget. And if you retire, you’ll need to adjust your budget to reflect your reduced income.

2. Change in income: Income changes can also impact your budget. If you get a raise, you may be able to save more money or spend more on discretionary items. However, if you lose your job, you’ll need to make some tough decisions about how to cut your spending.

3. Financial goals: Financial goals can also impact your budget. If you’re saving for a down payment on a house, you’ll need to make sure your budget includes enough money for that goal. And if you’re saving for retirement, you’ll need to factor in the cost of living in retirement.

The key to successful budgeting is to be flexible and adaptable. As your circumstances change, you need to be willing to adjust your budget accordingly. This will help you stay on track financially and achieve your goals.

Important Tips for being flexible and adaptable when it comes to budgeting:

Track your spending. This will help you see where your money is going and identify areas where you can cut back.

Set financial goals. This will give you something to work towards and help you stay motivated.

Be prepared for unexpected expenses. This could mean having an emergency fund or setting aside money each month for unexpected expenses.

Be willing to adjust your budget as needed. This could mean cutting back on spending, increasing your income, or both.

By following these tips, you can be sure that your budget is dynamic and will adapt to your changing circumstances. This will help you stay on track financially and achieve your goals.

2. Right Frequency for Reviewing Your Budget:

The frequency with which you should review your budget depends on your individual circumstances and financial situation. However, there are some general guidelines that can help you determine the right frequency for you.

Monthly reviews: Monthly reviews are a good option for people who have a lot of variable expenses, such as those who freelance or work in commission-based sales. Monthly reviews can help you track your spending and make sure you’re not overspending in any particular category.

Quarterly reviews: Quarterly reviews are a good option for people who have more stable income and expenses. Quarterly reviews can help you make sure your budget is still on track and that you’re on track to reach your financial goals.

pros and cons of different review frequencies:

Annual reviews: Annual reviews are a good option for people who have relatively stable income and expenses and who are not saving for any specific goals. Annual reviews can help you make sure your budget is still working for you and that you’re not missing any opportunities to save money.

Pros and Cons of different review frequencies:

Monthly reviews:

Pros:

Can help you track your spending and make sure you’re not overspending.

Can help you identify areas where you can save money.

Can help you stay on track with your financial goals.

Cons:

Can be time-consuming.

Can be difficult to keep up with if you have a lot of variable expenses.

Quarterly reviews:

Pros:

Can be less time-consuming than monthly reviews.

Can still help you track your spending and make sure you’re not overspending.

Can help you stay on track with your financial goals.

Cons:

May not be frequent enough to catch any major changes in your spending or income.

Annual reviews:

Pros:

Can be the least time-consuming option.

Can still help you track your spending and make sure you’re not overspending.

Can help you stay on track with your financial goals.

Cons:

May not be frequent enough to catch any major changes in your spending or income.

When choosing a review frequency, it’s important to consider your financial situation and preferences. If you have a lot of variable expenses, you may need to review your budget more frequently than someone with more stable income and expenses. And if you’re someone who likes to be organized and on top of things, you may prefer to review your budget more frequently than someone who is more laid-back.

Ultimately, the best frequency for reviewing your budget is the one that works best for you. There is no right or wrong answer, so experiment until you find a frequency that you’re comfortable with.

3. Signs that Indicate It’s Time to Adjust Your Budget:

Budgets are living documents that should be adjusted as your financial situation changes. Here are some signs that it’s time to adjust your budget:

Your income has changed: If you’ve gotten a raise or lost your job, your budget will need to be adjusted to reflect your new income. For example If you get a raise, you may be able to increase your savings or start investing. On the other hand If you lose your job, you may need to cut back on your expenses or find a way to increase your income.

Your expenses have changed: If you’ve had a baby, bought a new car, or started taking a night class, your budget will need to be adjusted to reflect your new expenses. If you have a baby, you’ll need to factor in the cost of childcare, diapers, and other baby expenses. In the same way If you buy a new car, you’ll need to factor in the cost of insurance, gas, and maintenance.

Your financial goals have changed: If you’ve decided to save for a down payment on a house or pay off your student loans, your budget will need to be adjusted to reflect your new goals.

consistently overspending: If you’re consistently overspending in one or more categories, your budget needs to be adjusted to help you reduce your spending.

You’re not on track to reach your financial goals: If you’re not on track to reach your financial goals, your budget needs to be adjusted to help you get back on track.

If you notice any of these signs, it’s time to take a look at your budget and make some adjustments. By adjusting your budget, you can ensure that your finances are on track and that you’re on track to reach your financial goals.

Additional tips for adjusting your budget:

Start by tracking your spending for a month or two. This will help you see where your money is going and identify areas where you can cut back.

Once you’ve tracked your spending, make a list of your financial goals. What are you saving for? When do you want to reach your goals?

Once you know your goals, start adjusting your budget to reflect them. This may mean increasing your savings, reducing your expenses, or both.

Be realistic about your budget. Don’t try to cut back too much too soon, or you’ll be more likely to give up.

Review your budget regularly and make adjustments as needed. Your financial situation is constantly changing, so your budget should change with it.

4. How to Effectively Adjust Your Budget:

Adjusting your budget can be a daunting task, but it doesn’t have to be. By following these tips, you can effectively adjust your budget and ensure that your finances are on track.

1. Start by tracking your spending for a month or two. This will help you see where your money is going and identify areas where you can cut back.

2. Once you’ve tracked your spending, make a list of your financial goals. What are you saving for? When do you want to reach your goals?

3. Once you know your goals, start adjusting your budget to reflect them. This may mean increasing your savings, reducing your expenses, or both.

4. Be realistic about your budget. Don’t try to cut back too much too soon, or you’re more likely to give up.

5. Review your budget regularly and make adjustments as needed. Your financial situation is constantly changing, so your budget should change with it.

How to modify budget categories and allocations:

Start by reviewing your budget and identifying areas where you can cut back. This could include things like eating out less, canceling unused subscriptions, or shopping around for cheaper car insurance.

Once you’ve identified areas where you can cut back, start reallocating those funds to your financial goals. This could mean increasing your savings, paying down debt, or saving for a specific purchase.

Be sure to factor in any upcoming expenses, such as annual insurance premiums or car registration fees. This will help you avoid overspending in the future.

Review your budget regularly and make adjustments as needed. Your financial situation is constantly changing, so your budget should change with it.

How to set new financial goals and priorities during the adjustment process:

Take some time to think about your short-term and long-term financial goals. What do you want to achieve with your money?

Once you know your goals, prioritize them. Which goals are most important to you?

Once you’ve prioritized your goals, adjust your budget to reflect them. This may mean increasing your savings for your down payment, paying down debt faster, or saving for a vacation.

Be flexible with your goals. Your financial situation may change, so be prepared to adjust your goals accordingly.

Here is some guidance on reallocating funds to ensure that essential expenses and savings are adequately addressed:

Start by listing all of your essential expenses, such as housing, food, transportation, and insurance.

Once you’ve listed your essential expenses, add up the total amount. This is the amount of money you need to allocate to these expenses each month.

Once you know how much money you need to allocate to essential expenses, start reallocating funds from other categories. This could mean eating out less, canceling unused subscriptions, or shopping around for cheaper car insurance.

Be sure to leave some money for savings. Even if it’s just a small amount, saving money each month will help you reach your financial goals.

5. Build and maintain an emergency fund.

What is an emergency fund?

An emergency fund is a pool of money that you set aside to cover unexpected expenses. This could include things like car repairs, medical bills, or job loss. Having an emergency fund can help you avoid going into debt when unexpected expenses arise.

How can an emergency fund help with budgeting adjustments?

An emergency fund can help you with budgeting adjustments in a few ways. First, it can give you the peace of mind to make changes to your budget without worrying about how you’re going to pay for unexpected expenses. Second, it can provide you with the financial flexibility to make changes to your budget without compromising your long-term financial goals.

For example, let’s say you have a budget that allocates $100 per month to entertainment. However, you realize that you can cut back on entertainment expenses and save that money instead. If you have an emergency fund, you can make this change to your budget without worrying about how you’re going to pay for unexpected expenses. You can use the money you save from entertainment to build up your emergency fund or to start saving for a long-term goal, such as a down payment on a house.

How to build and maintain an emergency fund:

The amount of money you need in an emergency fund will vary depending on your individual circumstances. However, a good rule of thumb is to have enough money to cover 3-6 months of living expenses.

There are a few different ways to build an emergency fund.

Start small and save consistently. You can start by setting aside a small amount of money each month. Even if you can only save $50 per month, it will add up over time. You can also look for ways to cut back on your expenses so that you can save more money.

Automate your savings. This will help you make sure that you’re saving money each month, even if you forget.

Look for ways to cut back on your expenses. This could mean eating out less, canceling unused subscriptions, or shopping around for cheaper car insurance.

Make sure your emergency fund is accessible. This means keeping it in a savings account or money market account where you can easily access it if you need it.

Once you have an emergency fund, it’s important to maintain it. This means adding money to your fund each month and making sure that the money is accessible in case of an emergency. It can help you avoid going into debt when unexpected expenses arise and it can give you the peace of mind to make changes to your budget without compromising your long-term financial goals.

6. Seeking Professional Guidance

Budgeting adjustments can be complex, especially if you are dealing with a lot of different variables. In these cases, it can be helpful to seek professional advice from a financial planner or advisor. A financial planner can help you assess your current financial situation, create a budget that meets your individual needs, and make adjustments to your budget as needed.

Scenarios where expert guidance can be beneficial in optimizing budget adjustments

When you are facing a major life change, such as a job loss or a new baby. These events can have a significant impact on your finances, and it can be helpful to have a financial planner who can help you make the necessary adjustments to your budget.

When you are trying to achieve a specific financial goal, such as saving for a down payment on a house or retirement. A financial planner can help you create a plan that will help you reach your goal on time and within your budget.

When you are simply feeling overwhelmed by your finances. If you are feeling lost or confused about your finances, a financial planner can help you get back on track.

you can find a reputable financial advisor by asking for referrals from friends, family, or colleagues. Do your research online. There are many websites that can help you compare financial advisors and find one who is a good fit for you. Once you have found a few potential advisors, schedule an interview with each one. This will give you a chance to ask questions and see if they are a good fit for you.

Some additional tips on finding a reputable financial advisor:

Make sure the advisor is a fiduciary. This means that they are legally obligated to act in your best interests.

Ask about the advisor’s fees. Financial advisors typically charge a fee for their services. Make sure you understand what the fees are and how they will be calculated.

Get everything in writing. Once you have chosen an advisor, make sure you get everything in writing. This includes the advisor’s fees, their investment philosophy, and their service agreement.

Conclusion

Key takeaways from this blog:

Regularly review your budget. This should be done at least once a month, but more often if your income or expenses are volatile.

Be open to making changes to your budget. If your income or expenses change, you may need to adjust your budget accordingly.

Be proactive in managing your budget. Don’t wait until you are in financial trouble to start managing your budget.

Track your spending. This will help you see where your money is going and identify areas where you can cut back.

Set financial goals. Having specific goals will help you stay motivated and on track.

Be realistic about your budget. Don’t try to cut back too much too soon, or you’ll be more likely to give up.

Seek professional guidance if needed. If you are struggling to manage your budget, a financial advisor can help you get back on track.

Remember, regular budget reviews and adjustments are vital for successful financial planning and achieving long-term financial goals. So don’t be afraid to make changes to your budget as needed. Your financial future will thank you for it.

Budgeting is essential for financial stability. Avoiding common budgeting mistakes is equally vital to maximize the benefits of budgeting. Tracking income and expenses helps us understand our financial habits and identify areas to save or invest. In this blog, we will discuss about 7 common budgeting mistakes and tricks to avoid it so that you can set yourself up for financial success. So, let’s delve into the world of budgeting and discover how to sidestep these common pitfalls!

1. Lack of Clear Goals and Planning:

Importance of setting clear financial goals:

Before you can create a budget, it’s important to set clear financial goals. What do you want to achieve with your budget? Are you saving for a down payment on a house? Paying off debt? Building an emergency fund? Once you know what you want to achieve, you can start creating a budget that will help you reach your goals.

Consequences of not having a plan in place:

If you don’t have a plan in place, it’s easy to overspend and not reach your financial goals. When you don’t have a budget, you’re more likely to spend money on things you don’t need. This can lead to debt, financial stress, and even bankruptcy.

Tips for setting realistic and achievable financial goals:

2.Failure to Track Expenses:

What is the Necessity of tracking expenses?

Tracking expenses is essential to understanding your spending habits and making informed financial decisions. When you track your expenses, you can see where your money is going and identify areas where you can cut back. You can also use your expense tracking data to set financial goals and track your progress towards those goals.

Implications of not tracking expenses:

If you don’t track your expenses, you’re more likely to overspend and not reach your financial goals. You may also underestimate your costs, which can lead to financial problems down the road. For example, if you don’t track your spending on eating out, you may not realize how much money you’re actually spending. This could lead to debt or financial stress.

Practical methods for tracking expenses:

In addition to understanding your spending habits, tracking expenses can also help you set financial goals and track your progress towards those goals. For example, if you track your spending on eating out, you may be able to identify areas where you can cut back. However, it’s important to choose a method of tracking expenses that works for you. If you don’t like using a mobile app, you can try using a spreadsheet or keeping a journal.

3.Ignoring Emergency Funds:

Importance of having an emergency fund:

An emergency fund is a savings account that you can use to cover unexpected expenses, such as a car repair, medical bill, or job loss. Having an emergency fund can help you avoid financial crises by giving you a financial cushion to fall back on when unexpected expenses arise.

Mistake of not prioritizing emergency savings in a budget:

One of the most common budgeting mistakes is not prioritizing emergency savings. When you create your budget, it’s important to set aside money each month for your emergency fund. This way, you’ll be prepared for unexpected expenses and won’t have to go into debt to cover them.

Strategies for building and maintaining an emergency fund:

There are many different strategies for building and maintaining an emergency fund. Some popular strategies include:

Start small: Don’t try to save too much too soon. Start by saving a small amount each month, such as $50 or $100.

Automate your savings: Set up an automatic transfer from your checking account to your savings account each month. This way, you won’t even have to think about it.

Use a high-yield savings account: A high-yield savings account will earn you more interest on your money, which will help your emergency fund grow faster.

Cut back on unnecessary expenses: If you’re struggling to save money for your emergency fund, you may need to cut back on unnecessary expenses. This could mean eating out less, canceling unused subscriptions, or finding cheaper ways to get around.

In addition to having an emergency fund, it’s also important to have a plan for how you’ll use it. For example, if you lose your job, you may need to use your emergency fund to cover your living expenses until you find a new job. However, it’s important to remember that an emergency fund is not a bottomless pit. You should only use it for unexpected expenses.

4.Overestimating Income or Underestimating Expenses:

Potential dangers of overestimating income and relying on unreliable sources:

When you overestimate your income, you’re setting yourself up for disappointment. You may end up spending more money than you have, which can lead to debt. Additionally, if you rely on unreliable sources of income, such as tips or commissions, you may not be able to accurately predict your income each month. This can make it difficult to create a budget that works for you.

Consequences of underestimating expenses and how it can lead to overspending:

Underestimating your expenses is another common budgeting mistake. When you underestimate your expenses, you’re more likely to overspend. This can happen because you’re not accounting for all of your expenses, or because you’re underestimating the cost of certain expenses. Overspending can lead to debt, financial stress, and even bankruptcy.

Tips for accurately estimating income and thoroughly considering all expenses:

To avoid these mistakes, it’s important to accurately estimate your income and thoroughly consider all of your expenses. Here are some tips:

Track your income and expenses for at least one month before you create your budget. This will give you a good idea of how much money you’re actually bringing in and spending each month.

Be realistic about your income. Don’t overestimate your income or rely on unreliable sources of income.

Consider all of your expenses. This includes both fixed expenses, such as rent and car payments, and variable expenses, such as food and entertainment.

Be prepared to adjust your budget as needed. Your income and expenses may change over time, so it’s important to be prepared to adjust your budget accordingly.

In addition to accurately estimating your income, it’s also important to thoroughly consider all of your expenses. For example, if you underestimate your grocery bill, you may end up overspending on food. However, it’s important to remember that your budget is a living document. It’s okay to adjust it as needed.

5.Failing to Adjust the Budget:

Importance of regularly reviewing and adjusting the budget as circumstances change:

A budget is a living document that should be regularly reviewed and adjusted as circumstances change. This is because your income and expenses can change over time, and you need to make sure that your budget reflects your current financial situation.

Mistake of sticking to a rigid budget without accounting for unexpected expenses or income changes:

If you stick to a rigid budget without accounting for unexpected expenses or income changes, you’re setting yourself up for failure. For example, if you have a car repair that you didn’t budget for, you may have to dip into your savings or go into debt.

How to adapt the budget effectively based on evolving financial situations:

Here are some tips on how to adapt your budget effectively based on evolving financial situations:

Review your budget regularly: At least once a month, review your budget to see if it’s still accurate. If your income or expenses have changed, you’ll need to adjust your budget accordingly.

Be prepared for unexpected expenses: Unexpected expenses are a part of life, so it’s important to be prepared for them. You can do this by setting aside an emergency fund or by having a credit card with a low interest rate.

Be flexible: Things change, so it’s important to be flexible with your budget. If your income decreases, you may need to cut back on your expenses. If your income increases, you may be able to save more money or splurge on something you’ve been wanting.

In addition to regularly reviewing your budget, you should also be prepared for unexpected expenses. For example, if your car breaks down, you’ll need to adjust your budget to account for the repair costs. However, it’s important to remember that you can’t always predict when unexpected expenses will occur.

6.Neglecting Debt Repayment:

Negative impact of neglecting debt repayment in a budget:

Neglecting debt repayment can have a negative impact on your budget in a number of ways. First, it can lead to increased interest charges, which can make your debt even harder to pay off. Second, it can lower your credit score, which can make it more difficult to get approved for loans or credit cards in the future. Third, it can put a strain on your finances, as you’ll have less money available to cover other expenses.

Mistake of not prioritizing debt repayment and its long-term consequences:

Not prioritizing debt repayment is a mistake that can have long-term consequences. If you don’t make regular payments on your debt, you may end up defaulting on your loans, which can damage your credit score even further. This can make it difficult to get approved for loans or credit cards in the future, which can make it harder to build your financial future.

Strategies for managing and reducing debt while maintaining a balanced budget:

Create a budget that includes a line item for debt repayment. This will help you track your progress and make sure you’re making regular payments on your debt.

Prioritize your debt repayment. Focus on paying off your highest-interest debt first, as this will save you money in the long run.

Consider consolidating your debt. This can help you save money on interest and make it easier to manage your payments.

Look for ways to reduce your expenses. This can free up more money to put towards debt repayment.

Get help from a financial advisor. If you’re struggling to manage your debt, a financial advisor can help you create a plan and stick to it.

In addition to creating a budget, you can also prioritize your debt repayment and look for ways to reduce your expenses. For example, if you have a credit card with a high-interest rate, you may want to consider consolidating your debt into a loan with a lower interest rate. However, it’s important to remember that there is no one-size-fits-all solution to debt management. The best strategy for you will depend on your individual circumstances.

7. Impulsive Spending and Lifestyle Inflation:

Common mistake of succumbing to impulsive spending and lifestyle inflation:

Impulsive spending is the act of buying something without thinking about it first. This can be caused by a number of factors, such as stress, boredom, or peer pressure. Lifestyle inflation is the gradual increase in your spending habits as your income increases. This can happen because you start to feel like you deserve to spend more money, or because you start to compare your lifestyle to others.

How these habits can hinder budgeting efforts and financial goals:

Impulsive spending can quickly derail your budget. If you’re not careful, you can easily overspend on things you don’t need. Lifestyle inflation can also be a problem, as it can lead to you spending more money than you can afford. This can make it difficult to reach your financial goals, such as saving for a down payment on a house or retirement.

Tips for curbing impulsive spending and avoiding unnecessary lifestyle inflation:

Plan your purchases in advance: Before you buy anything, take a few minutes to think about whether you really need it. If you’re not sure, wait a day or two before making a decision.

Set a budget and stick to it: This will help you track your spending and make sure you’re not overspending.

Avoid shopping when you’re tired, stressed, or bored: These are all times when you’re more likely to make impulse purchases.

Pay with cash: This will make you more aware of how much money you’re spending.

Wait 30 days before making a big purchase: This will give you time to think about whether you really want the item and if you can afford it.

Avoid comparing your lifestyle to others: Everyone’s financial situation is different, so don’t feel like you need to keep up with the Joneses.

In addition to planning your purchases in advance, you can also set a budget and stick to it. For example, if you’re tired, stressed, or bored, you’re more likely to make impulse purchases.

However, it’s important to remember that you can’t completely eliminate impulsive spending. It’s just important to be aware of it and try to curb it as much as possible.

explain Conclusion: Recap the main points discussed in the blog post regarding common budgeting mistakes to avoid. Emphasize the importance of learning from these mistakes to achieve financial success. Encourage readers to implement the suggested strategies and maintain discipline in their budgeting practices. use transition words, shorter sentences, and make short paragraph use

Conclusion:

To summarize, we discussed some of the most common budgeting mistakes to avoid. By learning from these mistakes, you can improve your financial situation and achieve your financial goals.

Key points to remember:

Set clear financial goals. What do you want to achieve with your budget? Are you saving for a down payment on a house? Paying off debt? Building an emergency fund?

Track your income and expenses. This will help you understand where your money is going and identify areas where you can cut back.

Create a budget that is realistic and achievable. Don’t set yourself up for failure by setting unrealistic goals.

Be prepared to adjust your budget as needed. Your income and expenses may change over time, so it’s important to be flexible with your budget.

Don’t neglect debt repayment. Making regular payments on your debt will help you save money in the long run and improve your credit score.

Be patient and disciplined. Budgeting takes time and effort, but it’s worth it in the long run.

I hope this blog post has been helpful. If you’re struggling to create a budget or stick to one, there are many resources available to help you. You can talk to a financial advisor, use a budgeting app, or join a budgeting support group.

The most important thing is to start somewhere. Even if you can only make a small change to your spending habits, it’s a step in the right direction. With time and effort, you can achieve your financial goals and build a strong financial future.

Do you ever wonder where your money goes? Do you feel like you’re constantly broke, even though you have a job? If so, you’re not alone. Millions of people struggle with their finances.

Welcome to our comprehensive guide on budgeting, where we delve into the world of financial management and empower you to take control of your money. Budgeting is more than just a way to track your expenses; it’s a powerful tool that can transform your financial life. Whether you’re looking to achieve specific financial goals, reduce debt, or simply gain a better understanding of your spending habits, budgeting is the key to unlocking financial success. In this blog, we will explore the importance of budgeting, different types of budgets, how to stick to your budget, and the wide-ranging benefits it offers. Get ready to embark on a journey towards financial empowerment as we navigate the ins and outs of budgeting and guide you towards a brighter financial future.

What is Budgeting?

Budgeting is a financial planning process that outlines how income will be earned and allocated to cover various expenses, savings, and investments. It involves strategies, estimating and tracking income sources, such as salaries, business profits, or government funds, and determining how that income will be distributed across different categories of expenses, such as housing, transportation, food, entertainment, and making adjustments as needed.

Benefits of Budgeting

Budgeting offers several benefits that contribute to effective financial management:

Improved Financial Control: Budgeting provides a clear picture of income and expenses, allowing individuals and entities to have better control over their finances. It helps avoid overspending, stay within financial limits, and prevent unnecessary debt accumulation.

Goal Achievement: By setting financial goals within a budget, individuals and entities can work towards specific objectives. Budgeting allows for the allocation of funds towards savings, debt repayment, investments, and other financial aspirations.

Debt Management: A budget assists in managing and reducing debt effectively. It helps prioritize debt repayments, avoid late payment fees, and develop strategies to pay off debt faster. This leads to improved financial health and reduced interest costs.

Savings and Emergency Preparedness: Budgeting encourages the habit of saving money. It facilitates the allocation of funds towards savings goals, such as building an emergency fund for unexpected expenses. This provides financial security and peace of mind.

Financial Awareness and Decision-Making: Budgeting promotes financial awareness by tracking income and expenses. It allows individuals and entities to identify spending patterns, analyze cost-saving opportunities, and make informed decisions about financial priorities.

Planning for the Future: Budgeting involves forecasting and planning for future financial needs and

Kickstart Budgeting

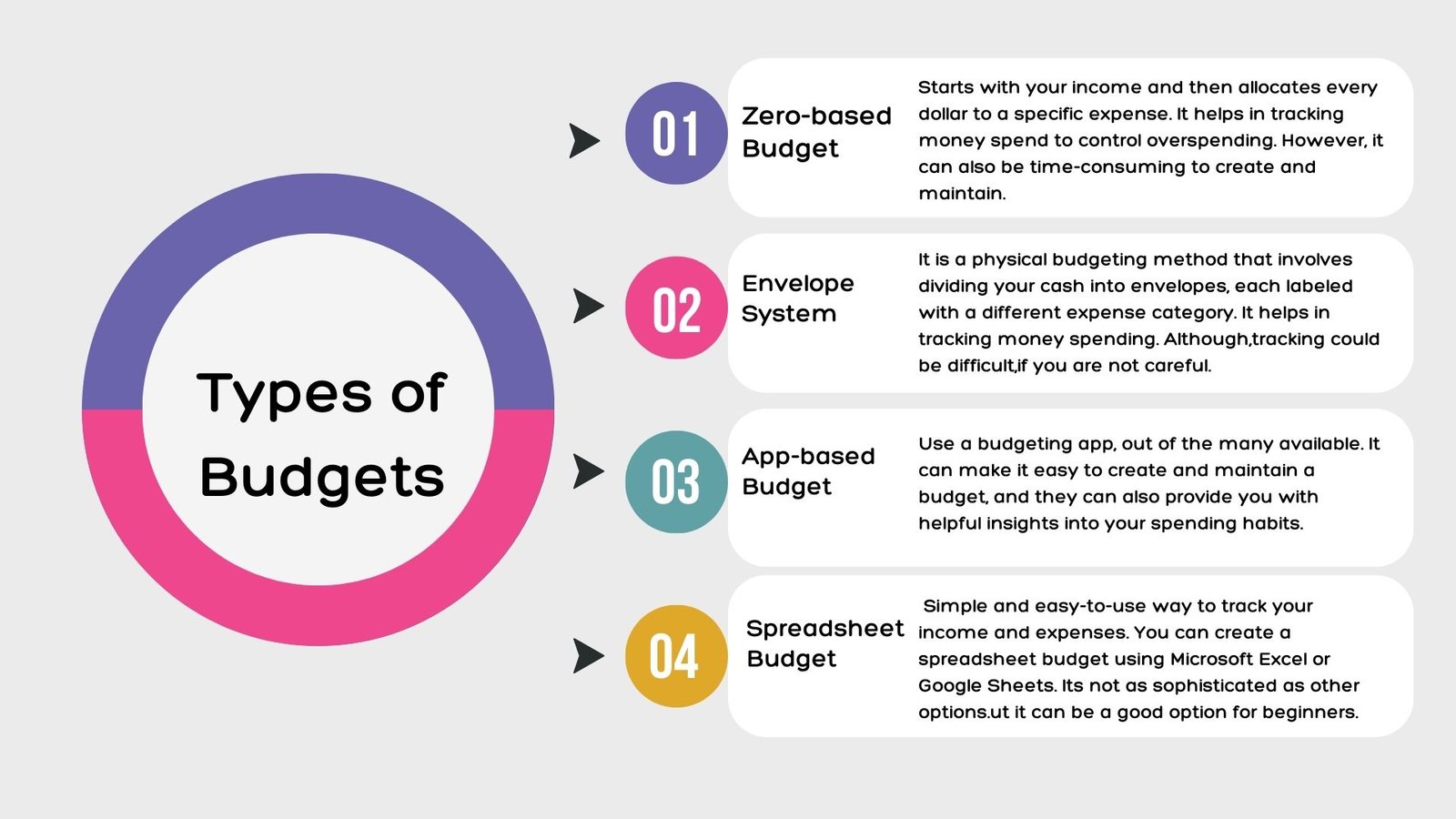

What are the different types of Budgets?

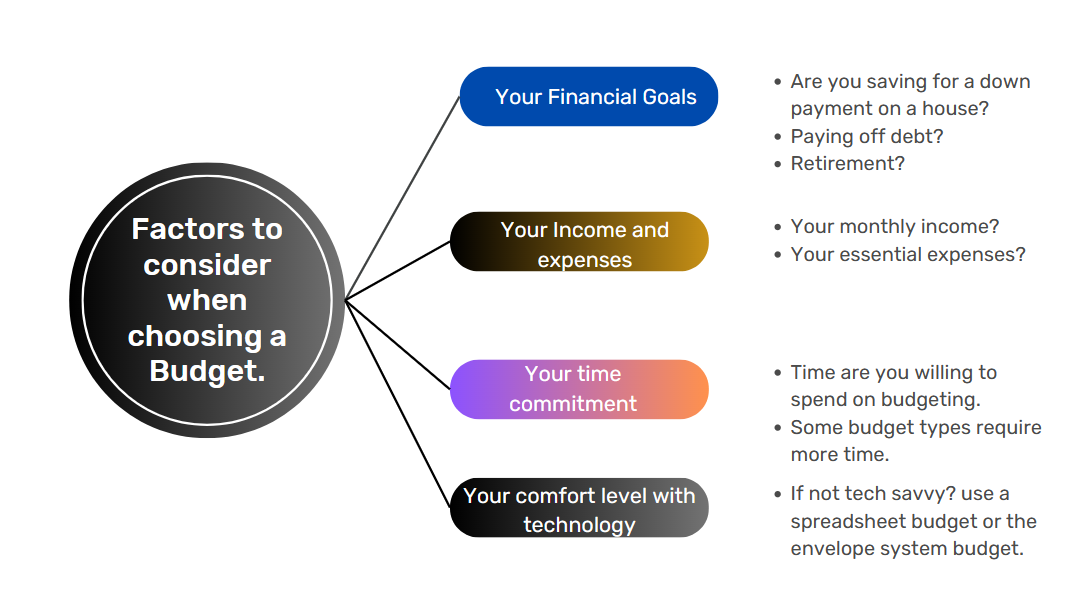

How to choose the right Budget type for you?

No matter what type of budget you choose, the most important thing is to stick to it. If you find that you are not sticking to your budget, you may need to adjust it or choose a different type of budget.

Important Budgeting tips for beginners

Here are some budgeting tips for beginners:

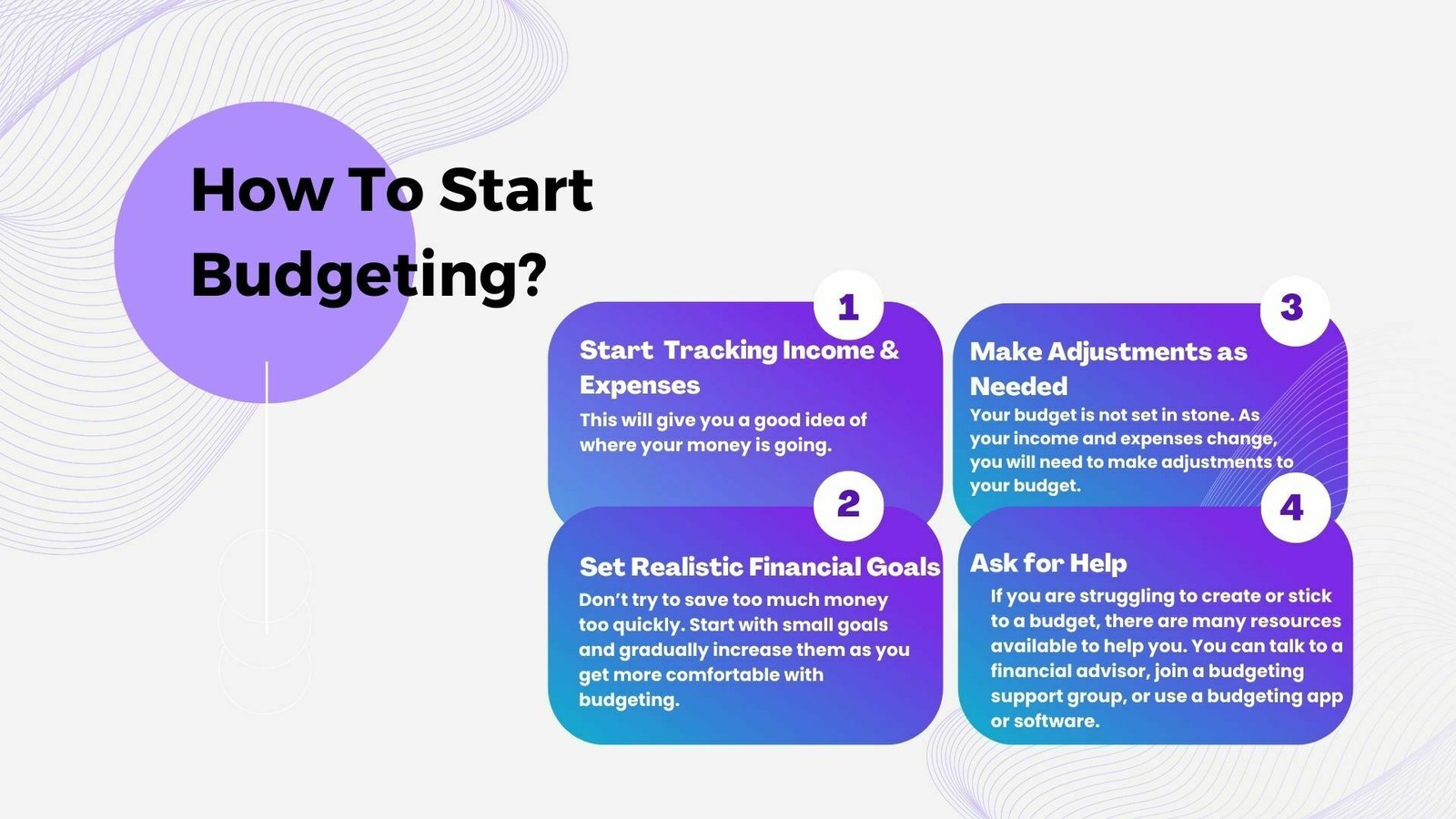

Start by tracking your income and expenses: This will give you a good idea of where your money is going. You can use a budgeting app, spreadsheet, or even just a piece of paper to track your spending.

Set realistic financial goals: Don’t try to save too much money too quickly. Start with small goals and gradually increase them as you get more comfortable with budgeting.

Make adjustments as needed: Your budget is not set in stone. As your income and expenses change, you will need to make adjustments to your budget.

Don’t be afraid to ask for help: If you are struggling to create or stick to a budget, there are many resources available to help you. You can talk to a financial advisor, join a budgeting support group, or use a budgeting app or software.

How to Stick to your budget

Automate your savings: If you can, set up automatic transfers from your checking account to your savings account. This will help you save money without even thinking about it.

Pay yourself first: When you get paid, put some money aside for savings before you pay any of your bills. This will help you stay on track with your financial goals.

Avoid impulse purchases: If you see something you want to buy, wait 24 hours before you buy it. This will give you time to think about whether you really need it or not.

Find ways to cut back on unnecessary expenses: Do you really need that expensive cable package? Could you cook more meals at home instead of eating out? There are many ways to cut back on your expenses without sacrificing your quality of life.

Reward yourself: When you stick to your budget, reward yourself with something you enjoy. This will help you stay motivated and on track.

Budgeting can be a challenge, but it is worth it. By following these tips, you can create a budget that will help you reach your financial goals and reduce stress.

Conclusion

Budgeting is an essential part of financial planning. It can help you track your spending, save for your goals, and stay out of debt. There are many different types of budgets, so you can find one that fits your individual needs and preferences.

If you’re new to budgeting, start by setting realistic goals. Then, track your spending for a month or two to get an idea of where your money is going. Once you know where your money is going, you can start to make adjustments to your budget.

Sticking to your budget can be challenging, but it’s worth it. When you stick to your budget, you’ll have financial peace of mind, increased savings, reduced debt, and better financial decision-making.

The benefits of budgeting extend beyond financial stability. It fosters financial awareness, enabling you to understand your spending habits, identify areas for improvement, and make adjustments as needed. Budgeting also promotes responsible financial behavior, helping you develop healthy money management habits that can positively impact your future.

Remember, budgeting is a dynamic process. It may require periodic adjustments as your financial circumstances change. Stay proactive, review your budget regularly, and adapt it to reflect your evolving needs and goals.

By embracing budgeting as a powerful tool, you are taking control of your financial future. So, start budgeting today and unlock the potential for financial freedom and success.

As we navigate the ever-changing financial landscape, it’s more important than ever to have a strong personal finance portfolio. Whether you’re just starting out in your career or you’re a seasoned investor, there are certain strategies you can use to build a solid financial foundation. In this article, we’ll explore seven essential tips for building your personal finance portfolio. From diversifying your investments to setting realistic goals, these tips will help you make smart decisions about your money and achieve financial success. So, whether you’re looking to grow your wealth or simply secure your future, read on to discover the key steps you need to take to build a strong personal finance portfolio.

Benefits of having a personal finance portfolio

A personal finance portfolio is a collection of investments, such as stocks, bonds, and mutual funds, that you own. Having a personal finance portfolio provides many benefits, including:

1. Long-term growth potential

A personal finance portfolio can provide long-term growth potential, as well as the potential for income through dividends and interest. By investing in a variety of assets, you can increase your chances of achieving long-term growth and financial stability.

2. Diversification

Diversifying your portfolio can help reduce risk. By investing in a variety of assets, you can decrease the impact of any single investment on your overall portfolio. This reduces the risk of losing all of your money if one investment performs poorly.

3. Flexibility

A personal finance portfolio provides flexibility and control over your investments. You can choose your investments based on your personal financial goals, risk tolerance, and investment horizon. This allows you to tailor your investments to your individual needs and preferences.

Understanding your financial goals

Before you start building your personal finance portfolio, it’s important to understand your financial goals. Your goals will help guide your investment decisions and determine your overall investment strategy. Some common financial goals include:

1. Saving for retirement

Retirement is a major financial goal for many people. To achieve this goal, you’ll need to have a solid investment strategy that provides long-term growth potential and income.

2. Saving for a down payment on a home

If you’re planning to buy a home, you’ll need to save for a down payment. This will require a mix of short-term and long-term investments, as you’ll need to balance your need for liquidity with your desire for long-term growth.

3. Paying off debt

If you have debt, such as credit card debt or student loans, paying it off should be a top financial goal. This may require you to prioritize debt repayment over investing until your debt is under control.

Diversification of your portfolio

Diversifying your portfolio is an essential part of building a strong personal finance portfolio. Diversification means investing in a variety of assets, such as stocks, bonds, and mutual funds, across different sectors and industries. This spreads your risk and helps protect your portfolio against market volatility.

1. Asset allocation

Asset allocation is the process of dividing your investments among different asset classes, such as stocks, bonds, and cash. This helps you balance risk and return by investing in assets with different levels of risk and potential return.

2. Sector diversification

Sector diversification involves investing in different sectors of the economy, such as technology, healthcare, and energy. This helps protect your portfolio against downturns in any one sector.

3. Geographic diversification

Geographic diversification involves investing in assets located in different regions of the world. This helps protect your portfolio against political and economic risk in any one country.

Investment options for your portfolio

There are many different investment options available to build your personal finance portfolio. Some common investment options include:

1. Stocks

Stocks represent ownership in a company and provide the potential for long-term growth. Stocks also pay dividends, which can provide income for investors.

2. Bonds

Bonds are debt securities issued by companies, municipalities, and governments. Bonds provide a fixed income stream and can help balance risk in a portfolio.

3. Mutual funds

Mutual funds are investment vehicles that pool money from many investors to purchase a diversified portfolio of stocks, bonds, and other assets. Mutual funds provide diversification and professional management.

Monitoring and adjusting your portfolio

Once you’ve built your personal finance portfolio, it’s important to monitor and adjust it as needed. This involves regularly reviewing your investments, rebalancing your portfolio, and making changes as necessary.

1. Regular reviews

Regularly reviewing your portfolio can help you stay on track and make necessary changes. This may involve reviewing your investments quarterly or annually, depending on your investment horizon and risk tolerance.

2. Rebalancing

Rebalancing involves adjusting your portfolio to maintain your desired asset allocation. This may involve selling assets that have performed well and investing in assets that have underperformed.

3. Making changes

Making changes to your portfolio may be necessary if your financial goals change or if market conditions warrant a change in strategy. This may involve adjusting your asset allocation, adding or removing investments, or changing your investment horizon.

Importance of seeking professional advice

Building a personal finance portfolio can be complex and time-consuming. Seeking professional advice can help you make informed investment decisions and achieve your financial goals. Some reasons to consider seeking professional advice from financial advisors include:

1. Expertise

Financial advisors have expertise in investing and can help you navigate the complex world of personal finance.

2. Objectivity

They can provide an objective perspective on your investments and help you make informed decisions based on your individual needs and goals.

3. Customization

Customize your investment strategy according to their insights to align with your specific requirements and preferences, enabling you to accomplish your financial objectives.

Tools and resources for building your personal finance portfolio

There are many tools and resources available to help you build your personal finance portfolio. Some common tools and resources include:

1. Online investment platforms

Online investment platforms, such as Robinhood and Betterment, provide easy access to a variety of investment options and can help you build a diversified portfolio.

2. Financial planning software

Financial planning software, such as Mint and Personal Capital, can help you track your expenses, manage your budget, and monitor your investments.

3. Investment research websites

Investment research websites, such as Morningstar and Seeking Alpha, provide valuable information and analysis on a variety of investments, helping you make informed investment decisions.

Common mistakes to avoid when building your portfolio

Building a personal finance portfolio can be challenging, and there are many common mistakes to avoid. Some common mistakes include:

1. Overconcentration

Overconcentration involves investing too heavily in one asset or sector, which can increase risk and reduce diversification.

2. Lack of diversification

Lack of diversification involves investing in too few assets, which can increase risk and reduce the potential for long-term growth.

3. Emotional investing

Emotional investing involves making investment decisions based on emotions, such as fear or greed, rather than on sound investment principles.

Conclusion

Building a strong personal finance portfolio takes time, effort, and careful planning. By understanding your financial goals, diversifying your portfolio, and seeking professional advice, you can make informed investment decisions and achieve financial success. Remember to regularly monitor and adjust your portfolio, avoid common mistakes, and take advantage of the many tools and resources available to help you build a strong personal finance portfolio.