In today’s highly competitive business landscape, it’s essential to keep a close eye on your share of the market. Knowing where you stand relative to your competitors can help you identify areas for improvement and capitalize on untapped opportunities. But how can you measure your share of the market accurately? That’s where metrics come in. By tracking the right metrics, you can gain valuable insights into your market position and stay ahead of the competition.

In this article, we’ll discuss the top five key metrics that you should be monitoring to measure your share of the market. From customer acquisition cost to lifetime value, we’ll cover the metrics that matter most and show you how to use them to make informed decisions about your business. So, whether you’re a startup or an established enterprise, read on to discover the metrics that will help you stay ahead of the game.

The importance of measuring share of market

Measuring the share of the market is essential for businesses to evaluate their market position. It helps them gauge their market share and identify opportunities to increase it. By tracking the market share, businesses can identify their strengths and weaknesses, which allows them to focus on their strengths and improve their weaknesses. Share of market is essential because it helps businesses understand their market position relative to their competitors. Without this knowledge, businesses cannot make informed decisions about where they should focus their efforts.

Understanding the 5 key metrics

To measure the share of the market accurately, businesses must track the right metrics. Here are the top five metrics that businesses should monitor:

Metric 1: Market share

Market share is the percentage of the total market that your business owns. It is calculated by dividing your business’s total sales by the total sales of all businesses in the market. For example, if your business’s total sales are $100,000, and the total sales of all businesses in the market are $1,000,000, your market share is 10%.

Measuring market share is important because it helps businesses understand their position relative to their competitors. If a business has a low market share, it may indicate that they need to increase their marketing efforts or improve their product offering.

Metric 2: Customer acquisition rate

Customer acquisition rate measures the rate at which a business acquires new customers. It is calculated by dividing the number of new customers by the total number of customers. For example, if a business acquires 50 new customers and has a total of 500 customers, the customer acquisition rate is 10%.

Measuring customer acquisition rate is important because it helps businesses evaluate their marketing strategies. If a business has a low customer acquisition rate, it may indicate that their marketing efforts are not effective.

Metric 3: Customer retention rate

Customer retention rate measures the rate at which a business retains its customers. It is calculated by subtracting the number of lost customers from the total number of customers and dividing the result by the total number of customers. For example, if a business has 500 customers at the beginning of the month, loses 50 customers during the month, and has 450 customers at the end of the month, the customer retention rate is 90%.

Measuring customer retention rate is important because it helps businesses understand their customer loyalty. If a business has a high customer retention rate, it may indicate that their products and services are meeting the needs of their customers.

Metric 4: Net promoter score (NPS)

Net promoter score (NPS) measures the likelihood of a customer recommending a business to others. It is calculated by subtracting the percentage of detractors (customers who would not recommend the business) from the percentage of promoters (customers who would recommend the business). For example, if 50% of customers are promoters, and 20% are detractors, the NPS is 30%.

Measuring NPS is important because it helps businesses understand the level of customer satisfaction and loyalty. A high NPS indicates that customers are satisfied with the business and are likely to recommend it to others.

Metric 5: Customer lifetime value (CLV)

Customer lifetime value (CLV) measures the total value that a customer brings to a business over their lifetime. It is calculated by multiplying the average value of a sale by the number of transactions per year and the average length of the customer relationship. For example, if the average value of a sale is $100, the number of transactions per year is 4, and the average length of the customer relationship is 5 years, the CLV is $2,000.

Measuring CLV is important because it helps businesses understand the value of their customers. By identifying customers with a high CLV, businesses can focus on retaining those customers and providing them with the best possible service.

How to calculate and analyze the metrics

To calculate the metrics, businesses need to gather data from various sources such as customer databases, sales reports, and customer surveys. Once the data is collected, businesses can use various tools such as Excel or Google Sheets to calculate the metrics.

To analyze the metrics, businesses should compare their results to industry benchmarks and track changes over time. By doing so, businesses can identify trends and opportunities for improvement.

Using the metrics to stay ahead of the competition.

By monitoring the five key metrics, businesses can gain valuable insights into their market position and stay ahead of the competition. For example, if a business has a low market share, they can focus on increasing their marketing efforts or improving their product offering. If a business has a low customer retention rate, they can focus on improving their customer service or product quality.

The metrics can also help businesses identify their strengths and weaknesses. For example, if a business has a high NPS, they can identify the factors that contribute to customer satisfaction and replicate them across their product offering.

Conclusion

Measuring the share of the market is essential for businesses to stay ahead of the competition. By tracking the right metrics, businesses can gain valuable insights into their market position and identify opportunities for improvement. The key metrics that businesses should monitor include market share, customer acquisition rate, customer retention rate, net promoter score (NPS), and customer lifetime value (CLV). By calculating and analyzing these metrics, businesses can make informed decisions about where to focus their efforts and stay ahead of the competition.

Budgeting is essential for financial stability. Avoiding common budgeting mistakes is equally vital to maximize the benefits of budgeting. Tracking income and expenses helps us understand our financial habits and identify areas to save or invest. In this blog, we will discuss about 7 common budgeting mistakes and tricks to avoid it so that you can set yourself up for financial success. So, let’s delve into the world of budgeting and discover how to sidestep these common pitfalls!

1. Lack of Clear Goals and Planning:

Importance of setting clear financial goals:

Before you can create a budget, it’s important to set clear financial goals. What do you want to achieve with your budget? Are you saving for a down payment on a house? Paying off debt? Building an emergency fund? Once you know what you want to achieve, you can start creating a budget that will help you reach your goals.

Consequences of not having a plan in place:

If you don’t have a plan in place, it’s easy to overspend and not reach your financial goals. When you don’t have a budget, you’re more likely to spend money on things you don’t need. This can lead to debt, financial stress, and even bankruptcy.

Tips for setting realistic and achievable financial goals:

2.Failure to Track Expenses:

What is the Necessity of tracking expenses?

Tracking expenses is essential to understanding your spending habits and making informed financial decisions. When you track your expenses, you can see where your money is going and identify areas where you can cut back. You can also use your expense tracking data to set financial goals and track your progress towards those goals.

Implications of not tracking expenses:

If you don’t track your expenses, you’re more likely to overspend and not reach your financial goals. You may also underestimate your costs, which can lead to financial problems down the road. For example, if you don’t track your spending on eating out, you may not realize how much money you’re actually spending. This could lead to debt or financial stress.

Practical methods for tracking expenses:

In addition to understanding your spending habits, tracking expenses can also help you set financial goals and track your progress towards those goals. For example, if you track your spending on eating out, you may be able to identify areas where you can cut back. However, it’s important to choose a method of tracking expenses that works for you. If you don’t like using a mobile app, you can try using a spreadsheet or keeping a journal.

3.Ignoring Emergency Funds:

Importance of having an emergency fund:

An emergency fund is a savings account that you can use to cover unexpected expenses, such as a car repair, medical bill, or job loss. Having an emergency fund can help you avoid financial crises by giving you a financial cushion to fall back on when unexpected expenses arise.

Mistake of not prioritizing emergency savings in a budget:

One of the most common budgeting mistakes is not prioritizing emergency savings. When you create your budget, it’s important to set aside money each month for your emergency fund. This way, you’ll be prepared for unexpected expenses and won’t have to go into debt to cover them.

Strategies for building and maintaining an emergency fund:

There are many different strategies for building and maintaining an emergency fund. Some popular strategies include:

Start small: Don’t try to save too much too soon. Start by saving a small amount each month, such as $50 or $100.

Automate your savings: Set up an automatic transfer from your checking account to your savings account each month. This way, you won’t even have to think about it.

Use a high-yield savings account: A high-yield savings account will earn you more interest on your money, which will help your emergency fund grow faster.

Cut back on unnecessary expenses: If you’re struggling to save money for your emergency fund, you may need to cut back on unnecessary expenses. This could mean eating out less, canceling unused subscriptions, or finding cheaper ways to get around.

In addition to having an emergency fund, it’s also important to have a plan for how you’ll use it. For example, if you lose your job, you may need to use your emergency fund to cover your living expenses until you find a new job. However, it’s important to remember that an emergency fund is not a bottomless pit. You should only use it for unexpected expenses.

4.Overestimating Income or Underestimating Expenses:

Potential dangers of overestimating income and relying on unreliable sources:

When you overestimate your income, you’re setting yourself up for disappointment. You may end up spending more money than you have, which can lead to debt. Additionally, if you rely on unreliable sources of income, such as tips or commissions, you may not be able to accurately predict your income each month. This can make it difficult to create a budget that works for you.

Consequences of underestimating expenses and how it can lead to overspending:

Underestimating your expenses is another common budgeting mistake. When you underestimate your expenses, you’re more likely to overspend. This can happen because you’re not accounting for all of your expenses, or because you’re underestimating the cost of certain expenses. Overspending can lead to debt, financial stress, and even bankruptcy.

Tips for accurately estimating income and thoroughly considering all expenses:

To avoid these mistakes, it’s important to accurately estimate your income and thoroughly consider all of your expenses. Here are some tips:

Track your income and expenses for at least one month before you create your budget. This will give you a good idea of how much money you’re actually bringing in and spending each month.

Be realistic about your income. Don’t overestimate your income or rely on unreliable sources of income.

Consider all of your expenses. This includes both fixed expenses, such as rent and car payments, and variable expenses, such as food and entertainment.

Be prepared to adjust your budget as needed. Your income and expenses may change over time, so it’s important to be prepared to adjust your budget accordingly.

In addition to accurately estimating your income, it’s also important to thoroughly consider all of your expenses. For example, if you underestimate your grocery bill, you may end up overspending on food. However, it’s important to remember that your budget is a living document. It’s okay to adjust it as needed.

5.Failing to Adjust the Budget:

Importance of regularly reviewing and adjusting the budget as circumstances change:

A budget is a living document that should be regularly reviewed and adjusted as circumstances change. This is because your income and expenses can change over time, and you need to make sure that your budget reflects your current financial situation.

Mistake of sticking to a rigid budget without accounting for unexpected expenses or income changes:

If you stick to a rigid budget without accounting for unexpected expenses or income changes, you’re setting yourself up for failure. For example, if you have a car repair that you didn’t budget for, you may have to dip into your savings or go into debt.

How to adapt the budget effectively based on evolving financial situations:

Here are some tips on how to adapt your budget effectively based on evolving financial situations:

Review your budget regularly: At least once a month, review your budget to see if it’s still accurate. If your income or expenses have changed, you’ll need to adjust your budget accordingly.

Be prepared for unexpected expenses: Unexpected expenses are a part of life, so it’s important to be prepared for them. You can do this by setting aside an emergency fund or by having a credit card with a low interest rate.

Be flexible: Things change, so it’s important to be flexible with your budget. If your income decreases, you may need to cut back on your expenses. If your income increases, you may be able to save more money or splurge on something you’ve been wanting.

In addition to regularly reviewing your budget, you should also be prepared for unexpected expenses. For example, if your car breaks down, you’ll need to adjust your budget to account for the repair costs. However, it’s important to remember that you can’t always predict when unexpected expenses will occur.

6.Neglecting Debt Repayment:

Negative impact of neglecting debt repayment in a budget:

Neglecting debt repayment can have a negative impact on your budget in a number of ways. First, it can lead to increased interest charges, which can make your debt even harder to pay off. Second, it can lower your credit score, which can make it more difficult to get approved for loans or credit cards in the future. Third, it can put a strain on your finances, as you’ll have less money available to cover other expenses.

Mistake of not prioritizing debt repayment and its long-term consequences:

Not prioritizing debt repayment is a mistake that can have long-term consequences. If you don’t make regular payments on your debt, you may end up defaulting on your loans, which can damage your credit score even further. This can make it difficult to get approved for loans or credit cards in the future, which can make it harder to build your financial future.

Strategies for managing and reducing debt while maintaining a balanced budget:

Create a budget that includes a line item for debt repayment. This will help you track your progress and make sure you’re making regular payments on your debt.

Prioritize your debt repayment. Focus on paying off your highest-interest debt first, as this will save you money in the long run.

Consider consolidating your debt. This can help you save money on interest and make it easier to manage your payments.

Look for ways to reduce your expenses. This can free up more money to put towards debt repayment.

Get help from a financial advisor. If you’re struggling to manage your debt, a financial advisor can help you create a plan and stick to it.

In addition to creating a budget, you can also prioritize your debt repayment and look for ways to reduce your expenses. For example, if you have a credit card with a high-interest rate, you may want to consider consolidating your debt into a loan with a lower interest rate. However, it’s important to remember that there is no one-size-fits-all solution to debt management. The best strategy for you will depend on your individual circumstances.

7. Impulsive Spending and Lifestyle Inflation:

Common mistake of succumbing to impulsive spending and lifestyle inflation:

Impulsive spending is the act of buying something without thinking about it first. This can be caused by a number of factors, such as stress, boredom, or peer pressure. Lifestyle inflation is the gradual increase in your spending habits as your income increases. This can happen because you start to feel like you deserve to spend more money, or because you start to compare your lifestyle to others.

How these habits can hinder budgeting efforts and financial goals:

Impulsive spending can quickly derail your budget. If you’re not careful, you can easily overspend on things you don’t need. Lifestyle inflation can also be a problem, as it can lead to you spending more money than you can afford. This can make it difficult to reach your financial goals, such as saving for a down payment on a house or retirement.

Tips for curbing impulsive spending and avoiding unnecessary lifestyle inflation:

Plan your purchases in advance: Before you buy anything, take a few minutes to think about whether you really need it. If you’re not sure, wait a day or two before making a decision.

Set a budget and stick to it: This will help you track your spending and make sure you’re not overspending.

Avoid shopping when you’re tired, stressed, or bored: These are all times when you’re more likely to make impulse purchases.

Pay with cash: This will make you more aware of how much money you’re spending.

Wait 30 days before making a big purchase: This will give you time to think about whether you really want the item and if you can afford it.

Avoid comparing your lifestyle to others: Everyone’s financial situation is different, so don’t feel like you need to keep up with the Joneses.

In addition to planning your purchases in advance, you can also set a budget and stick to it. For example, if you’re tired, stressed, or bored, you’re more likely to make impulse purchases.

However, it’s important to remember that you can’t completely eliminate impulsive spending. It’s just important to be aware of it and try to curb it as much as possible.

explain Conclusion: Recap the main points discussed in the blog post regarding common budgeting mistakes to avoid. Emphasize the importance of learning from these mistakes to achieve financial success. Encourage readers to implement the suggested strategies and maintain discipline in their budgeting practices. use transition words, shorter sentences, and make short paragraph use

Conclusion:

To summarize, we discussed some of the most common budgeting mistakes to avoid. By learning from these mistakes, you can improve your financial situation and achieve your financial goals.

Key points to remember:

Set clear financial goals. What do you want to achieve with your budget? Are you saving for a down payment on a house? Paying off debt? Building an emergency fund?

Track your income and expenses. This will help you understand where your money is going and identify areas where you can cut back.

Create a budget that is realistic and achievable. Don’t set yourself up for failure by setting unrealistic goals.

Be prepared to adjust your budget as needed. Your income and expenses may change over time, so it’s important to be flexible with your budget.

Don’t neglect debt repayment. Making regular payments on your debt will help you save money in the long run and improve your credit score.

Be patient and disciplined. Budgeting takes time and effort, but it’s worth it in the long run.

I hope this blog post has been helpful. If you’re struggling to create a budget or stick to one, there are many resources available to help you. You can talk to a financial advisor, use a budgeting app, or join a budgeting support group.

The most important thing is to start somewhere. Even if you can only make a small change to your spending habits, it’s a step in the right direction. With time and effort, you can achieve your financial goals and build a strong financial future.

Do you ever wonder where your money goes? Do you feel like you’re constantly broke, even though you have a job? If so, you’re not alone. Millions of people struggle with their finances.

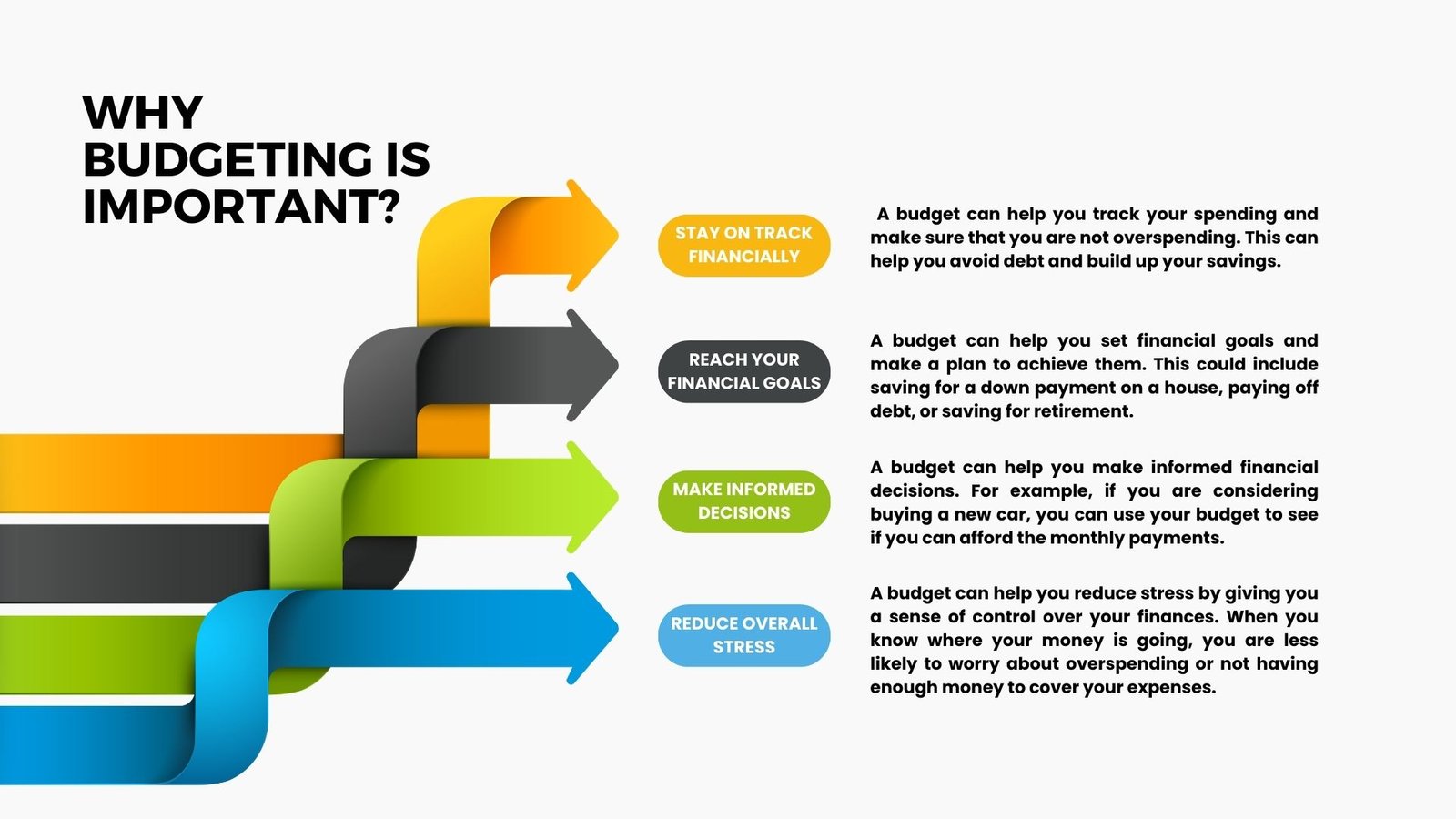

Welcome to our comprehensive guide on budgeting, where we delve into the world of financial management and empower you to take control of your money. Budgeting is more than just a way to track your expenses; it’s a powerful tool that can transform your financial life. Whether you’re looking to achieve specific financial goals, reduce debt, or simply gain a better understanding of your spending habits, budgeting is the key to unlocking financial success. In this blog, we will explore the importance of budgeting, different types of budgets, how to stick to your budget, and the wide-ranging benefits it offers. Get ready to embark on a journey towards financial empowerment as we navigate the ins and outs of budgeting and guide you towards a brighter financial future.

What is Budgeting?

Budgeting is a financial planning process that outlines how income will be earned and allocated to cover various expenses, savings, and investments. It involves strategies, estimating and tracking income sources, such as salaries, business profits, or government funds, and determining how that income will be distributed across different categories of expenses, such as housing, transportation, food, entertainment, and making adjustments as needed.

Benefits of Budgeting

Budgeting offers several benefits that contribute to effective financial management:

Improved Financial Control: Budgeting provides a clear picture of income and expenses, allowing individuals and entities to have better control over their finances. It helps avoid overspending, stay within financial limits, and prevent unnecessary debt accumulation.

Goal Achievement: By setting financial goals within a budget, individuals and entities can work towards specific objectives. Budgeting allows for the allocation of funds towards savings, debt repayment, investments, and other financial aspirations.

Debt Management: A budget assists in managing and reducing debt effectively. It helps prioritize debt repayments, avoid late payment fees, and develop strategies to pay off debt faster. This leads to improved financial health and reduced interest costs.

Savings and Emergency Preparedness: Budgeting encourages the habit of saving money. It facilitates the allocation of funds towards savings goals, such as building an emergency fund for unexpected expenses. This provides financial security and peace of mind.

Financial Awareness and Decision-Making: Budgeting promotes financial awareness by tracking income and expenses. It allows individuals and entities to identify spending patterns, analyze cost-saving opportunities, and make informed decisions about financial priorities.

Planning for the Future: Budgeting involves forecasting and planning for future financial needs and

Kickstart Budgeting

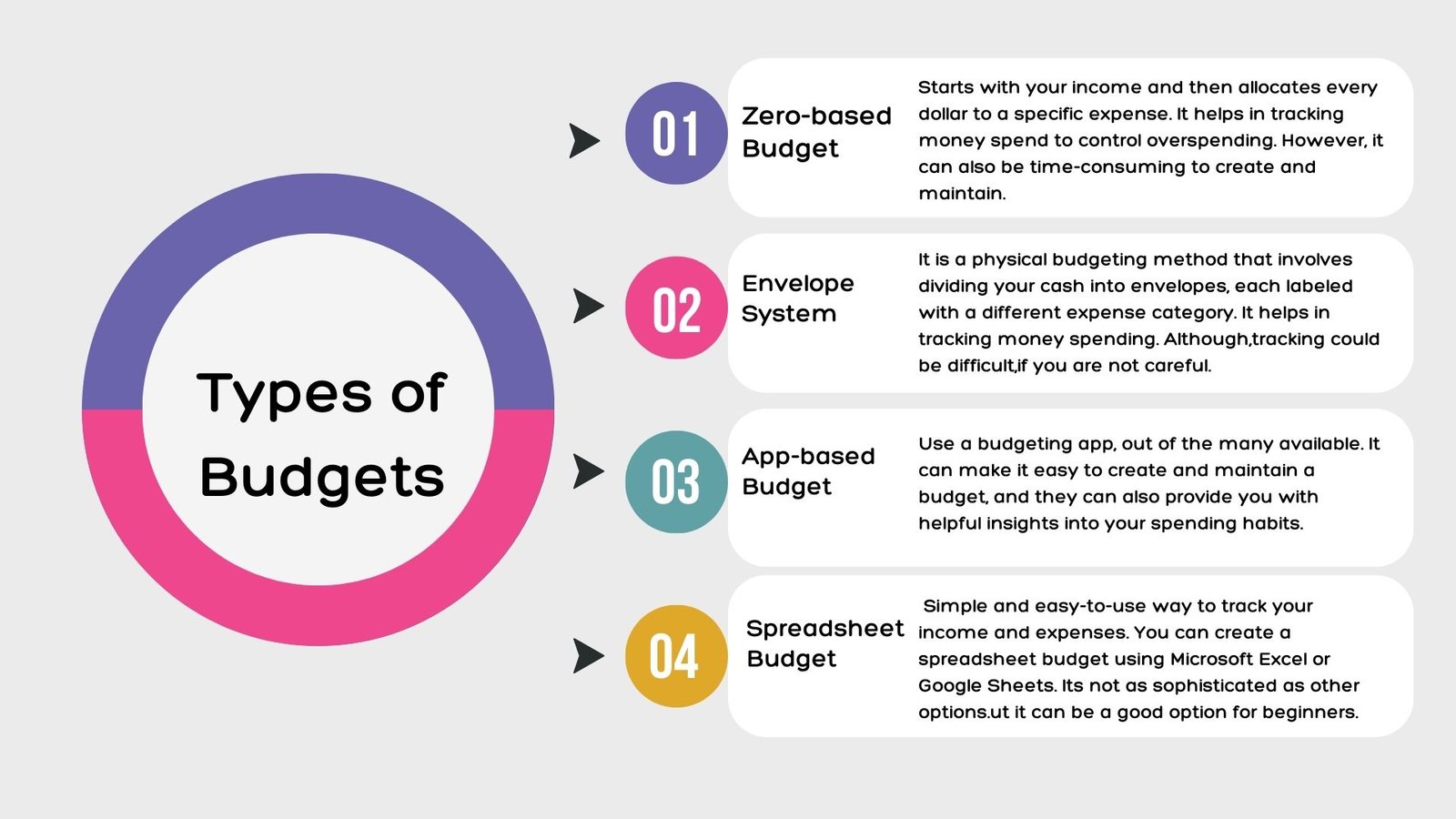

What are the different types of Budgets?

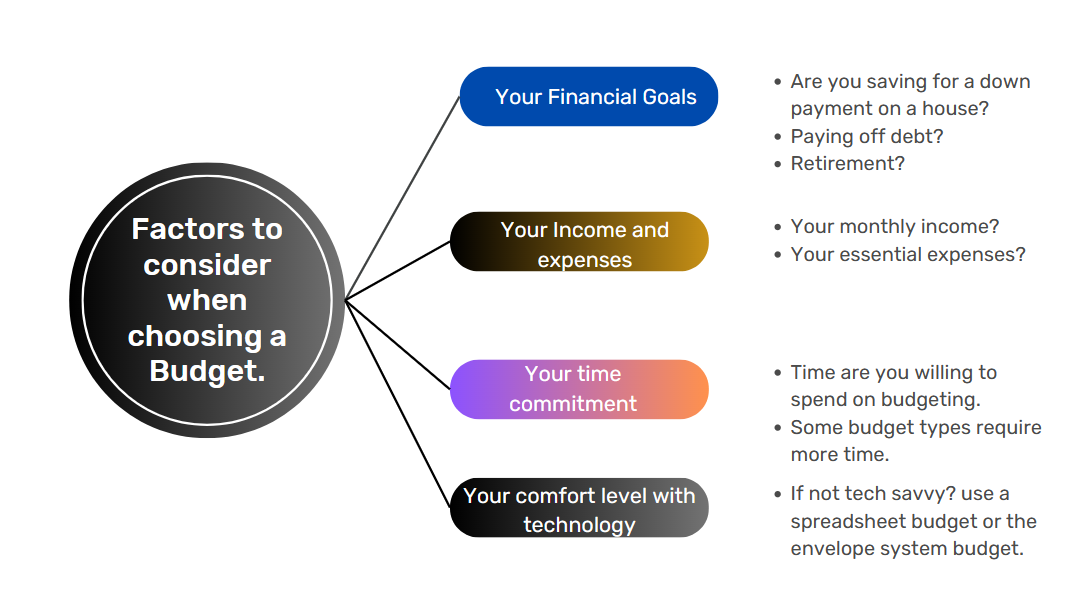

How to choose the right Budget type for you?

No matter what type of budget you choose, the most important thing is to stick to it. If you find that you are not sticking to your budget, you may need to adjust it or choose a different type of budget.

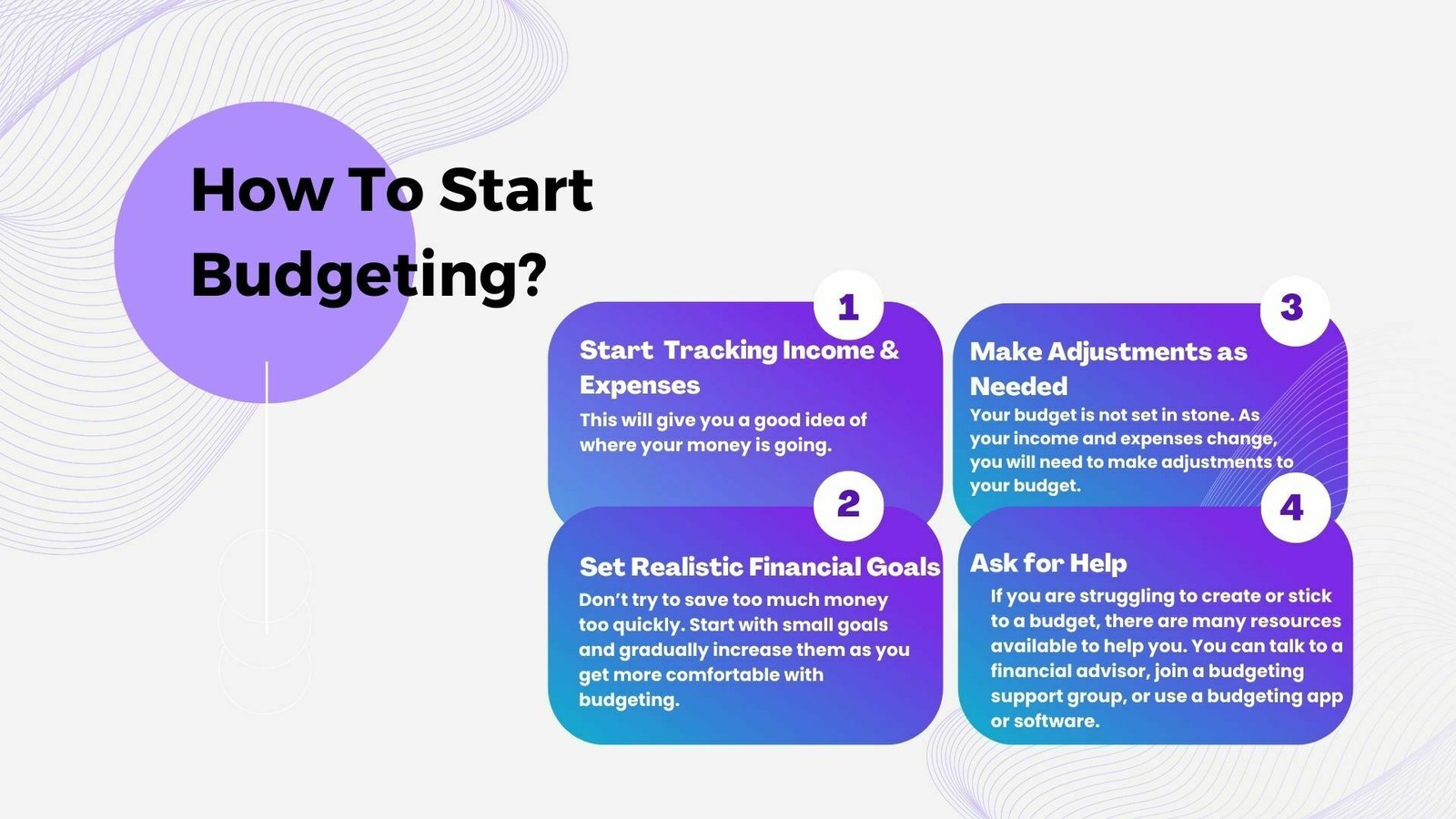

Important Budgeting tips for beginners

Here are some budgeting tips for beginners:

Start by tracking your income and expenses: This will give you a good idea of where your money is going. You can use a budgeting app, spreadsheet, or even just a piece of paper to track your spending.

Set realistic financial goals: Don’t try to save too much money too quickly. Start with small goals and gradually increase them as you get more comfortable with budgeting.

Make adjustments as needed: Your budget is not set in stone. As your income and expenses change, you will need to make adjustments to your budget.

Don’t be afraid to ask for help: If you are struggling to create or stick to a budget, there are many resources available to help you. You can talk to a financial advisor, join a budgeting support group, or use a budgeting app or software.

How to Stick to your budget

Automate your savings: If you can, set up automatic transfers from your checking account to your savings account. This will help you save money without even thinking about it.

Pay yourself first: When you get paid, put some money aside for savings before you pay any of your bills. This will help you stay on track with your financial goals.

Avoid impulse purchases: If you see something you want to buy, wait 24 hours before you buy it. This will give you time to think about whether you really need it or not.

Find ways to cut back on unnecessary expenses: Do you really need that expensive cable package? Could you cook more meals at home instead of eating out? There are many ways to cut back on your expenses without sacrificing your quality of life.

Reward yourself: When you stick to your budget, reward yourself with something you enjoy. This will help you stay motivated and on track.

Budgeting can be a challenge, but it is worth it. By following these tips, you can create a budget that will help you reach your financial goals and reduce stress.

Conclusion

Budgeting is an essential part of financial planning. It can help you track your spending, save for your goals, and stay out of debt. There are many different types of budgets, so you can find one that fits your individual needs and preferences.

If you’re new to budgeting, start by setting realistic goals. Then, track your spending for a month or two to get an idea of where your money is going. Once you know where your money is going, you can start to make adjustments to your budget.

Sticking to your budget can be challenging, but it’s worth it. When you stick to your budget, you’ll have financial peace of mind, increased savings, reduced debt, and better financial decision-making.

The benefits of budgeting extend beyond financial stability. It fosters financial awareness, enabling you to understand your spending habits, identify areas for improvement, and make adjustments as needed. Budgeting also promotes responsible financial behavior, helping you develop healthy money management habits that can positively impact your future.

Remember, budgeting is a dynamic process. It may require periodic adjustments as your financial circumstances change. Stay proactive, review your budget regularly, and adapt it to reflect your evolving needs and goals.

By embracing budgeting as a powerful tool, you are taking control of your financial future. So, start budgeting today and unlock the potential for financial freedom and success.

As we navigate the ever-changing financial landscape, it’s more important than ever to have a strong personal finance portfolio. Whether you’re just starting out in your career or you’re a seasoned investor, there are certain strategies you can use to build a solid financial foundation. In this article, we’ll explore seven essential tips for building your personal finance portfolio. From diversifying your investments to setting realistic goals, these tips will help you make smart decisions about your money and achieve financial success. So, whether you’re looking to grow your wealth or simply secure your future, read on to discover the key steps you need to take to build a strong personal finance portfolio.

Benefits of having a personal finance portfolio

A personal finance portfolio is a collection of investments, such as stocks, bonds, and mutual funds, that you own. Having a personal finance portfolio provides many benefits, including:

1. Long-term growth potential

A personal finance portfolio can provide long-term growth potential, as well as the potential for income through dividends and interest. By investing in a variety of assets, you can increase your chances of achieving long-term growth and financial stability.

2. Diversification

Diversifying your portfolio can help reduce risk. By investing in a variety of assets, you can decrease the impact of any single investment on your overall portfolio. This reduces the risk of losing all of your money if one investment performs poorly.

3. Flexibility

A personal finance portfolio provides flexibility and control over your investments. You can choose your investments based on your personal financial goals, risk tolerance, and investment horizon. This allows you to tailor your investments to your individual needs and preferences.

Understanding your financial goals

Before you start building your personal finance portfolio, it’s important to understand your financial goals. Your goals will help guide your investment decisions and determine your overall investment strategy. Some common financial goals include:

1. Saving for retirement

Retirement is a major financial goal for many people. To achieve this goal, you’ll need to have a solid investment strategy that provides long-term growth potential and income.

2. Saving for a down payment on a home

If you’re planning to buy a home, you’ll need to save for a down payment. This will require a mix of short-term and long-term investments, as you’ll need to balance your need for liquidity with your desire for long-term growth.

3. Paying off debt

If you have debt, such as credit card debt or student loans, paying it off should be a top financial goal. This may require you to prioritize debt repayment over investing until your debt is under control.

Diversification of your portfolio

Diversifying your portfolio is an essential part of building a strong personal finance portfolio. Diversification means investing in a variety of assets, such as stocks, bonds, and mutual funds, across different sectors and industries. This spreads your risk and helps protect your portfolio against market volatility.

1. Asset allocation

Asset allocation is the process of dividing your investments among different asset classes, such as stocks, bonds, and cash. This helps you balance risk and return by investing in assets with different levels of risk and potential return.

2. Sector diversification

Sector diversification involves investing in different sectors of the economy, such as technology, healthcare, and energy. This helps protect your portfolio against downturns in any one sector.

3. Geographic diversification

Geographic diversification involves investing in assets located in different regions of the world. This helps protect your portfolio against political and economic risk in any one country.

Investment options for your portfolio

There are many different investment options available to build your personal finance portfolio. Some common investment options include:

1. Stocks

Stocks represent ownership in a company and provide the potential for long-term growth. Stocks also pay dividends, which can provide income for investors.

2. Bonds

Bonds are debt securities issued by companies, municipalities, and governments. Bonds provide a fixed income stream and can help balance risk in a portfolio.

3. Mutual funds

Mutual funds are investment vehicles that pool money from many investors to purchase a diversified portfolio of stocks, bonds, and other assets. Mutual funds provide diversification and professional management.

Monitoring and adjusting your portfolio

Once you’ve built your personal finance portfolio, it’s important to monitor and adjust it as needed. This involves regularly reviewing your investments, rebalancing your portfolio, and making changes as necessary.

1. Regular reviews

Regularly reviewing your portfolio can help you stay on track and make necessary changes. This may involve reviewing your investments quarterly or annually, depending on your investment horizon and risk tolerance.

2. Rebalancing

Rebalancing involves adjusting your portfolio to maintain your desired asset allocation. This may involve selling assets that have performed well and investing in assets that have underperformed.

3. Making changes

Making changes to your portfolio may be necessary if your financial goals change or if market conditions warrant a change in strategy. This may involve adjusting your asset allocation, adding or removing investments, or changing your investment horizon.

Importance of seeking professional advice

Building a personal finance portfolio can be complex and time-consuming. Seeking professional advice can help you make informed investment decisions and achieve your financial goals. Some reasons to consider seeking professional advice from financial advisors include:

1. Expertise

Financial advisors have expertise in investing and can help you navigate the complex world of personal finance.

2. Objectivity

They can provide an objective perspective on your investments and help you make informed decisions based on your individual needs and goals.

3. Customization

Customize your investment strategy according to their insights to align with your specific requirements and preferences, enabling you to accomplish your financial objectives.

Tools and resources for building your personal finance portfolio

There are many tools and resources available to help you build your personal finance portfolio. Some common tools and resources include:

1. Online investment platforms

Online investment platforms, such as Robinhood and Betterment, provide easy access to a variety of investment options and can help you build a diversified portfolio.

2. Financial planning software

Financial planning software, such as Mint and Personal Capital, can help you track your expenses, manage your budget, and monitor your investments.

3. Investment research websites

Investment research websites, such as Morningstar and Seeking Alpha, provide valuable information and analysis on a variety of investments, helping you make informed investment decisions.

Common mistakes to avoid when building your portfolio

Building a personal finance portfolio can be challenging, and there are many common mistakes to avoid. Some common mistakes include:

1. Overconcentration

Overconcentration involves investing too heavily in one asset or sector, which can increase risk and reduce diversification.

2. Lack of diversification

Lack of diversification involves investing in too few assets, which can increase risk and reduce the potential for long-term growth.

3. Emotional investing

Emotional investing involves making investment decisions based on emotions, such as fear or greed, rather than on sound investment principles.

Conclusion

Building a strong personal finance portfolio takes time, effort, and careful planning. By understanding your financial goals, diversifying your portfolio, and seeking professional advice, you can make informed investment decisions and achieve financial success. Remember to regularly monitor and adjust your portfolio, avoid common mistakes, and take advantage of the many tools and resources available to help you build a strong personal finance portfolio.

Investment trends play a crucial role in determining where to allocate your money. Staying updated on these trends is essential for maximizing returns and making informed investment decisions. In this blog post, we will explore the investment landscape of 2023, highlighting key sectors, regions, and strategies to help you navigate the market successfully.

Current Economic Landscape

To make informed investment choices, it is important to analyze the global economy in 2023. Several factors, such as interest rates, geopolitical events, and technological advancements, can significantly impact investment opportunities.

Emerging Industries and Technologies

In 2023, certain sectors and industries show promising growth potential. Renewable energy, driven by the increasing focus on sustainability, offers exciting investment opportunities. Additionally, artificial intelligence, machine learning, e-commerce, and online retail are experiencing significant growth, making them attractive sectors to consider.

Geographical Investment Opportunities

Investors should explore regions with growth potential in 2023. The Asia-Pacific, Latin America, and Africa are emerging as hotspots for investment. Within these regions, specific countries offer unique investment prospects due to their economic growth, political stability, and infrastructure development.

Sustainable and Impact Investing

There is a rising interest in socially responsible investing. Sustainable investing focuses on companies that prioritize environmental, social, and governance (ESG) practices. Impact investing, on the other hand, seeks investments that generate positive social and environmental impacts alongside financial returns.

Alternative investments

Alternative investments, such as commodities, managed futures, and real estate, are becoming increasingly popular as investors seek to diversify their portfolios and reduce their risk. These investments are not as correlated to traditional asset classes like stocks and bonds, which can help to protect your portfolio during periods of market volatility.

Tech stocks

Technology stocks have been some of the best-performing investments in recent years, and they are likely to continue to be a popular choice in 2023. The technology sector is constantly innovating, and there are many new and exciting companies that are still in the early stages of growth.

Healthcare

The healthcare sector is another area that is expected to see strong growth in the coming years. The global population is aging, and there is a growing demand for healthcare services. This trend is likely to continue in the years to come, making healthcare stocks a good investment for the long term.

Renewables

Renewable energy is becoming increasingly affordable and accessible, making it a good investment for those who are looking to reduce their carbon footprint. The cost of solar and wind power has fallen dramatically in recent years, and these technologies are becoming more competitive with traditional fossil fuels. This trend is likely to continue in the years to come, making renewable energy stocks a good investment for the long term.

Cryptocurrency and Blockchain

The cryptocurrency market continues to evolve in 2023, with new opportunities and risks. Investors should carefully consider the potential of blockchain technology and its impact on various industries. However, caution and thorough research are necessary when investing in cryptocurrencies due to their inherent volatility.

Real Estate and Property Investment

The real estate market presents attractive investment options. It is crucial to understand the current trends, such as urbanization, demographic shifts, and emerging property markets. Different types of property investments, including residential, commercial, and real estate investment trusts (REITs), offer diversification possibilities. You can also refer our post on Real state in India.

Risk Management and Diversification

Diversifying your investment portfolio is essential for mitigating risks. Allocating investments across different asset classes, industries, and regions helps balance potential losses and gains. Adopting risk management strategies, such as setting stop-loss orders and regularly reviewing portfolio performance, is vital for long-term success.

Conclusion

In summary, understanding investment trends is vital for making informed decisions and maximizing returns. By analyzing the current economic landscape, exploring emerging industries and technologies, considering geographical opportunities, and incorporating sustainable investing principles, you can position your investments for success in 2023. Additionally, being mindful of cryptocurrency and blockchain developments, real estate investment prospects, and practicing risk management and diversification strategies will contribute to your overall investment success. Remember to conduct thorough research and seek professional advice when necessary to make the best investment choices for your financial future.

Disclaimer: This post is only for educational purposes not an investment advice.

Welcome to our comprehensive guide on budgeting strategies for beginners. In this blog post, we will provide you with valuable insights and practical tips to help you navigate the world of budgeting with ease.

Understanding Budgeting Basics

Budgeting is the process of managing your money effectively. By creating a budget, you gain control over your finances and make informed decisions about how you spend and save. It’s important to understand the benefits of budgeting and dispel any misconceptions. It’s even more important during current times of inflation.

Assessing Your Financial Situation

To start budgeting, you need to assess your financial situation. Calculate your income and identify your expenses. Categorize your expenses into different areas such as housing, transportation, groceries, and entertainment. Analyze your spending patterns to identify areas where you can make adjustments.

Setting Financial Goals

Setting clear financial goals is essential for effective budgeting. Determine your short-term and long-term goals, whether it’s saving for a vacation, paying off debt, or building an emergency fund. Prioritize your goals based on their importance and feasibility.

Different Budgeting Strategies

There are various budgeting strategies you can choose from. One popular method is the 50/30/20 rule, which allocates 50% of your income to needs, 30% to wants, and 20% to savings. Another strategy is the envelope budgeting method, where you allocate cash to different envelopes for each spending category. Zero-based budgeting and the pay yourself first strategy are also effective approaches.

Creating a Personalized Budget

Create a personalized budget that aligns with your financial goals and lifestyle. Determine a realistic budget by considering your income and expenses. Allocate funds to different categories based on their priority. Don’t forget to allocate money for savings and debt repayment.

Tracking Expenses and Monitoring Progress

Tracking your expenses is crucial for staying on top of your budget. Use tools and apps to simplify expense tracking. Regularly review and adjust your budget as needed. Celebrate milestones along the way to stay motivated.

Dealing with Financial Challenges

Budgeting may come with challenges, but there are strategies to overcome them. Reduce expenses by finding cost-cutting opportunities. Prepare for unexpected financial emergencies by having an emergency fund in place.

Additional Tips for Successful Budgeting

Consider ways to increase your income, such as taking on a side gig or negotiating a raise. Avoid common budgeting mistakes, like underestimating expenses or not accounting for irregular costs. Seek professional advice if you need guidance on complex financial matters.

Conclusion

Congratulations! You now have a comprehensive understanding of budgeting strategies for beginners. Start implementing what you’ve learned and take control of your finances. Remember, budgeting is a continuous process, so regularly review and adjust your budget as needed. By practicing good budgeting habits, you’ll be on your way to achieving financial stability and reaching your goals.

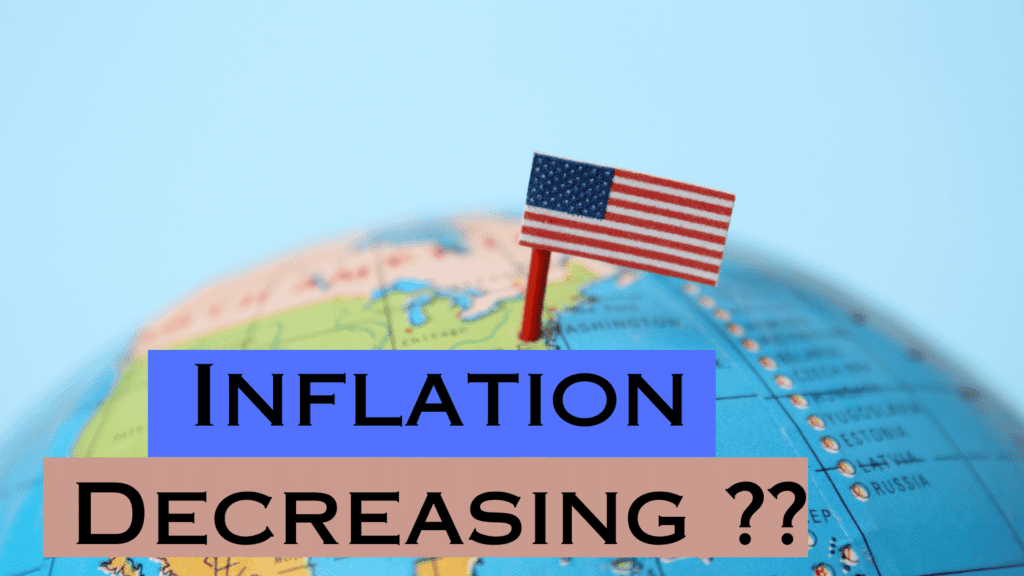

Welcome to our blog post where we delve into the economic trends and changes observed in the United States between June 2022 and June 2023. By analyzing key economic parameters, with a particular focus on inflation, we can gain valuable insights into the country’s economic landscape during this period. From currency stability to stock market fluctuations, and from GDP growth rates to unemployment levels, let’s explore the trends that have shaped the United States’ economic performance over the past year.

Yearly Comparison: June 2022 vs. June 2023

Based on United States Indicators (tradingeconomics.com) data, comparing the June 2022 and June 2023 data for the United States, we can observe the following trends on economic parameters, particularly regarding inflation:

1. Currency: The value of the US dollar (USD) has remained relatively stable at 104 in June 2022 and June 2023 at 102.

2. Stock Market: The stock market index has slightly decreased from 31,501 points in June 2022 to 34,299 points in June 2023. This suggests some volatility and fluctuations in the stock market during this period.

3. GDP Growth Rate: The GDP growth rate has increased from -1.5% in June 2022 to 1.3% in June 2023. This indicates a recovery in economic growth over the year.

4. GDP Annual Growth Rate: The GDP annual growth rate has decreased from 3.5% in June 2022 to 1.6% in June 2023. This suggests a slower pace of economic expansion over the year.

5. Unemployment Rate: The unemployment rate has slightly increased from 3.6% in June 2022 to 3.7% in June 2023. This indicates a small uptick in unemployment levels.

6. Inflation Rate: The inflation rate has decreased from 8.6% in June 2022 to 4% in June 2023. This suggests a decline in the rate of price increases and a moderation in inflation.

7. Interest Rate: The interest rate has increased from 1.75% in June 2022 to 5.25% in June 2023. This indicates a significant tightening of monetary policy to control inflation and manage economic conditions.

8. Balance of Trade: The balance of trade has improved, with the deficit decreasing from -87,077 USD million in June 2022 to -74.55 USD billion in June 2023.

9. Government Debt to GDP: The government debt to GDP ratio has increased from 137% in June 2022 to 129% in June 2023. This indicates a higher level of debt relative to the size of the economy.

10. Business Confidence: Business confidence has slightly decreased from 56.1 points in June 2022 to 46.9 points in June 2023. This suggests a slightly less optimistic outlook among businesses.

Conclusion

In conclusion, the analysis of economic data from June 2022 to June 2023 provides a comprehensive overview of the United States’ economic condition. The trends observed in various parameters, especially regarding inflation, shed light on the country’s economic landscape. While the US dollar remained stable, the stock market experienced fluctuations. The GDP growth rate indicated a recovery, albeit at a slower pace, and the unemployment rate saw a slight increase. Notably, the decrease in the inflation rate and the tightening of the interest rate demonstrated efforts to manage economic conditions. Although there was an improvement in GDP growth and a moderation in inflation, challenges persisted in terms of unemployment levels and government debt. It’s crucial to recognize that economic conditions are influenced by a myriad of factors, both domestically and globally. These trends provide a valuable snapshot of the economic situation during the respective periods and pave the way for further analysis and discussion on the United States’ economic trajectory.

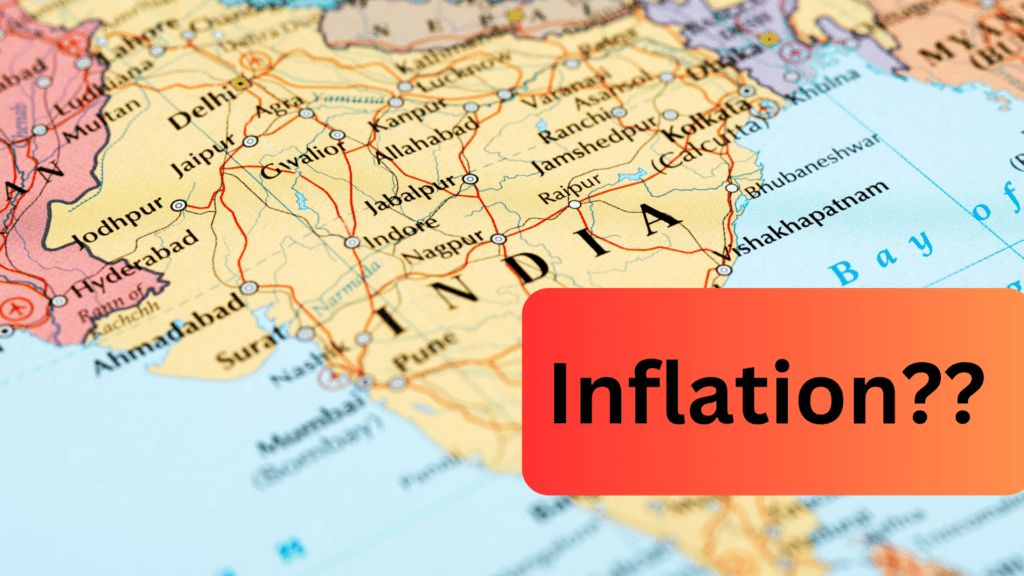

Inflation is a critical economic parameter that significantly impacts a country’s overall financial health. In this blog post, we will analyze the yearly comparison of economic indicators in India, specifically focusing on the June 2022 and June 2023 data. By examining various factors such as currency value, stock market performance, GDP growth rate, unemployment rate, inflation rate, interest rate, cash reserve ratio, and business confidence, we can gain valuable insights into the current state of India’s economy.

Currency: In June 2022, the Indian currency (INR) stood at 78.97 against other major currencies. However, in June 2023, it depreciated to 81.91, indicating a decline in its value. We will explore the potential reasons behind this fluctuation.

Stock Market: The stock market index experienced substantial growth, surging from 53,019 points in June 2022 to 63,385 points in June 2023. This positive trend reflects market sentiment and provides insights into the performance of India’s stock market.

GDP Growth Rate: Although there was a slight decline in the GDP growth rate from 0.8% in June 2022 to 0.69% in June 2023, the annual growth rate demonstrated improvement, increasing from 4.1% to 6.1%.

Unemployment Rate: India’s unemployment rate remained relatively stable, experiencing a slight decrease from 7.8% in June 2022 to 7.5% in June 2023.

Inflation Rate: A noteworthy observation is the decrease in the inflation rate from 7.04% in June 2022 to 4.25% in June 2023.

Interest Rate: The interest rate saw an increase from 4.9% in June 2022 to 6.5% in June 2023. This tightening of monetary policy aims to control inflation and stimulate savings.

Cash Reserve Ratio: The cash reserve ratio remained constant at 4.5% throughout both periods. This ratio plays a crucial role in determining the proportion of bank deposits that banks must maintain as reserves with the central bank.

Business Confidence: Business confidence showed a slight decline, decreasing from 135 points in June 2022 to 126 points in June 2023.

Conclusion: India’s economy presents a mixed picture based on the analysis of these economic indicators. The GDP annual growth rate has improved, and inflation has decreased substantially. However, challenges remain in terms of unemployment. By examining these trends and their interaction with global economic factors, we can gain a better understanding of India’s current economic situation. It is important to note that economic conditions are influenced by both domestic and international factors, and this analysis offers a snapshot of the economic situation during the respective periods.

ChatGPT is a powerful tool that has the potential to revolutionize the way we interact with AI. It is still early days, but Chat GPT is already showing great promise. What is Chat GPT? Join us on this insightful journey of the possibilities and limitations of Powerful Chat GPT in shaping the future of AI-driven conversations and a Game-Changer in AI Assistants

What is Chat GPT?

Chat GBT is a large language model chatbot developed by OpenAI. It can generate text, translate languages, write different kinds of creative content, and answer your questions in an informative way. Chat GBT is still under development, but it has learned to perform many kinds of tasks, including * Following your instructions and completing your requests thoughtfully. * Using its knowledge to answer your questions in a comprehensive and informative way, even if they are open ended, challenging, or strange. * Generating different creative text formats of text content, like poems, code, scripts, musical pieces, email, letters, etc.

How does Chat GPT work?

ChatGPT is a large language model chatbot developed by OpenAI. It is trained on a massive dataset of text and code, including books, articles, code, and other forms of text. ChatGPT can generate text, translate languages, write different kinds of creative content, and answer your questions in an informative way.

ChatGPT works by using a technique called “transformer”. Transformers are a type of neural network that are particularly good at learning long-range dependencies in text. This means that ChatGPT can understand the context of a conversation and generate responses that are relevant and coherent.

When you interact with ChatGPT, it first tries to understand what you are asking or saying. It does this by breaking down your input into smaller units, such as words and phrases. It then looks for patterns in these units and uses these patterns to generate a response.

ChatGPT’s responses are not always perfect. It can sometimes make mistakes, such as generating text that is grammatically incorrect or factually inaccurate. However, ChatGPT is still under development and is constantly learning and improving.

Let’s see how it works:

Data collection or Pre-training: ChatGPT is trained on a massive dataset of text and code. This dataset includes books, articles, code, and other forms of text. This pre-training phase involves predicting the next word in a sentence, which helps the model learn grammar, facts, reasoning abilities, and contextual understanding.

Data preprocessing: The data is preprocessed to remove noise and make it easier for ChatGPT to learn from. This includes removing punctuation, stop words, and other unnecessary information.

Model training or Fine-tuning: After pre-training, the model is fine-tuned on a specific dataset that is carefully generated with human feedback. In the case of Chat GPT, this fine-tuning involves exposing the model to conversations or dialogue-like interactions. ChatGPT is trained using a technique called “supervised learning”. This involves feeding the model a large number of examples of text and code, along with the correct responses. Human AI trainers provide conversations, playing both user and AI assistant roles. The model is trained to predict appropriate responses based on the provided dialogue history.

Model evaluation: Once the model is trained, it is evaluated on a set of test data. This data is not used to train the model, so it can be used to measure how well the model performs on new data.

Input processing: When a user interacts with Chat GPT, the input is processed and tokenized into smaller units, such as words or subwords. These tokens are then passed to the model as input.

Model deployment or Response generation: Once the model is evaluated and deemed to be performing well, it is deployed so that users can interact with it. Chat GPT generates a response by predicting the most probable tokens based on the given dialogue history and the context provided by the user. The output tokens are then decoded and transformed into human-readable text.

Iterative conversation: Chat GPT can handle multi-turn conversations by keeping track of the dialogue history. The model takes into account the previous conversation turns to generate more coherent and contextually relevant responses.

ChatGPT is a powerful tool that can be used for a variety of purposes. It can be used to chat with users in a natural and engaging way, answer questions in a comprehensive and informative way, and generate creative text formats, such as poems, code, scripts, musical pieces, email, letters, etc.

It’s important to note that while Chat GPT performs impressively in generating human-like responses, it has limitations. It may sometimes produce incorrect or nonsensical answers, be overly verbose, or fail to ask clarifying questions for ambiguous queries. Users should critically evaluate and verify the information provided by the model.

What are the benefits of using Chat GPT?

Chat GBT can be used for a variety of purposes, including:

Natural language interaction: Chat GPT enables natural language conversation, allowing users to interact with the model in a conversational manner. This makes it easier and more intuitive for users to communicate their queries or requests.

Versatility: Chat GPT can be used across various domains and applications. It can answer questions, provide explanations, generate text, offer suggestions, and engage in open-ended conversations. Its versatility makes it adaptable to different use cases.

Knowledge repository: Chat GPT has been trained on a vast amount of text data, allowing it to possess a wide range of knowledge and information. It can provide answers to factual questions, discuss historical events, explain concepts, and offer insights on various topics.

24/7 availability: As an AI model, Chat GPT can operate continuously without the need for breaks. It is available 24/7, allowing users to access information or engage in conversations at any time, making it convenient and accessible.

Scalability: Chat GPT can handle multiple conversations simultaneously, making it scalable for serving large numbers of users concurrently. It can efficiently manage and respond to multiple queries or requests in real-time.

Language support: Chat GPT supports multiple languages, enabling users from different linguistic backgrounds to interact with the model in their preferred language. This expands its reach and usability on a global scale.

Continuous learning: The underlying GPT model can be fine-tuned and improved over time with additional data. This allows the model to learn from user interactions and adapt to provide better responses and suggestions in the future.

Assistance and automation: Chat GPT can assist users in various tasks, such as providing recommendations, helping with problem-solving, or automating certain processes. It can offer personalized suggestions based on user preferences or historical interactions.

User-friendly interface integration: Chat GPT can be integrated into various platforms, applications, or websites, providing a user-friendly interface for users to interact with. This integration facilitates seamless communication and enhances user experience.

Customer service: Chat GBT can be used to answer customer questions, provide support, and resolve issues.

Education: Chat GBT can be used to provide personalized tutoring, help students with their homework, and create interactive learning experiences.

Entertainment: Chat GBT can be used to play games, tell stories, and create other forms of entertainment.

Business: Chat GBT can be used to generate marketing materials, create presentations, and automate tasks.

What are the limitations of Chat GPT?

ChatGPT is a powerful tool, but it does have some limitations. Here are some of the limitations of Chat GPT:

Lack of real-time information: Chat GPT does not have access to real-time information or the ability to browse the internet. Its responses are based on the knowledge it has learned from the pre-training phase and the fine-tuning dataset. As a result, it may not have the most up-to-date or accurate information, especially regarding rapidly changing events or recent developments.

Sensitivity to input phrasing: Chat GPT is highly sensitive to the phrasing and wording of input queries. Small changes in the question structure or phrasing can sometimes result in different or incorrect responses. Users may need to experiment with different ways of asking the same question to obtain the desired answer.

Inability to verify sources: Chat GPT does not possess the ability to verify the accuracy or credibility of the information it generates. It may provide plausible-sounding answers even if they are incorrect, biased, or unsupported. Users should independently verify the information from reliable sources.

Tendency to guess: When faced with ambiguous queries or insufficient context, Chat GPT often tries to guess the user’s intent and provide a response. This can lead to inaccurate or nonsensical answers. It may not prompt for clarifications when the input is unclear.

Generation of verbose responses: Chat GPT sometimes produces excessively long or verbose responses that contain unnecessary repetition or irrelevant information. This can make the output less concise and may require users to extract the relevant details from the generated text.

Lack of commonsense reasoning: While Chat GPT can generate coherent responses based on its training data, it may struggle with common sense reasoning and logical consistency. It can occasionally provide answers that are technically correct but don’t align with real-world knowledge or common sense.

Limited ethical understanding: Chat GPT lacks a deep understanding of ethics and may produce responses that are biased, offensive, or harmful. It is important to review and moderate the generated content to ensure it aligns with ethical guidelines and standards.

Dependence on training data: Chat GPT’s responses are based on the patterns and information present in the training data it was exposed to. If the training data is biased, contains inaccuracies, or lacks diversity, the model may exhibit similar biases or limitations in its responses.

It is crucial to use Chat GPT responsibly, critically evaluate its outputs, and consider its limitations when relying on its generated information or responses.

Overall, ChatGPT is a powerful tool, but it is important to be aware of its limitations. ChatGPT should not be used as a replacement for human judgment or critical thinking. It is important to use ChatGPT with caution and to be aware of the potential risks.

what is the future of Chat GPT?

The future of ChatGPT is bright. ChatGPT is a powerful tool that has the potential to revolutionize the way we interact with technology. ChatGPT can be used for a variety of purposes, including customer service, marketing, education, and personal use.

As ChatGPT continues to develop, it will become more and more sophisticated. It will be able to generate text that is more human-like, and it will be able to answer questions in a more comprehensive and informative way. ChatGPT will also be able to generate creative text formats, such as poems, code, scripts, musical pieces, email, letters, etc.

ChatGPT has the potential to change the way we live and work. It can make our lives easier and more efficient. It can also help us to learn and grow. The future of ChatGPT is bright, and it is an exciting time to be involved in the development of this technology.

Here are some specific examples of how ChatGPT could be used in the future:

Customer service: ChatGPT could be used to provide customer service by answering questions, resolving issues, and providing support. This could free up human customer service representatives to focus on more complex issues.

Marketing: ChatGPT could be used to create marketing materials, such as blog posts, social media posts, and email campaigns. This could help businesses reach a wider audience and generate more leads.

Education: ChatGPT could be used to create educational materials, such as lessons, quizzes, and games. This could help students learn new concepts and skills in a fun and engaging way.

Personal use: ChatGPT could be used for personal purposes, such as writing letters, creating stories, and generating ideas. This could help individuals express themselves creatively and achieve their goals.

Overall, ChatGPT has the potential to be a powerful tool that can benefit businesses and individuals alike. As ChatGPT continues to develop, it will become more and more sophisticated and will be able to be used for a wider variety of purposes.

Conclusion

In this blog, we have explored the limitless possibilities of ChatGPT. We have seen how it can be used to hold engaging and informative conversations, generate different creative text formats, translate languages, and answer your questions in an informative way.

We have also seen how ChatGPT is being used to make a positive impact on the world. For example, it is being used to help people learn new languages, write better content, and be more productive.

As ChatGPT continues to develop, it is likely that we will see even more amazing things from it. It is a truly revolutionary technology that has the potential to change the world.

I hope you enjoyed this blog on ChatGPT. If you have any questions or comments, please feel free to leave them below.

Inflation is a term we often hear, but what does it really mean? In simple terms, inflation refers to the increase in the general price level of goods and services over time. This rise in prices can have a significant impact on your finances, eroding the purchasing power of your hard-earned money. However, there are ways you can protect yourself from the effects of inflation. In this blog post, we will explore some practical tips to help safeguard your financial well-being.

Tips for Protecting Yourself from Inflation

1. Increase your income

One effective way to combat the effects of inflation is to find ways to increase your income. This may involve seeking a promotion, exploring additional job opportunities, or even starting a side business. By boosting your earnings, you can better keep up with rising prices and maintain your standard of living.

2. Cut your expenses

Reducing your expenses is another crucial step in protecting yourself from inflation. Analyze your budget and identify areas where you can make cuts. It might mean sacrificing certain luxuries or finding more cost-effective alternatives for your daily needs. By living within your means and spending wisely, you can minimize the impact of inflation on your savings.

3. Invest in assets that appreciate in value

Investing in assets that have the potential to appreciate in value faster than inflation is a strategic way to preserve your wealth. Consider diversifying your portfolio with investments such as stocks, real estate, or other assets that historically outpace inflation. These investments can help your money grow and maintain its purchasing power over time.

4. Diversify your investments

Diversification is key to mitigating risks in your investment portfolio. By spreading your investments across different asset classes, such as stocks, bonds, and commodities, you can minimize the impact if one particular investment underperforms. Diversification provides a level of protection during times of economic uncertainty and helps safeguard against the erosive effects of inflation.

5. Stay informed about inflation

Knowledge is power when it comes to protecting yourself from inflation. Stay informed about economic indicators and trends that impact inflation. Keep an eye on news and updates from reliable sources, and educate yourself about financial strategies that can help you navigate inflationary periods effectively. The more you know, the better equipped you’ll be to make informed decisions about your finances.

Conclusion

Inflation can pose challenges to your financial well-being, but by taking proactive measures, you can safeguard your money against its effects. By increasing your income, cutting expenses, investing wisely, diversifying your portfolio, and staying informed, you can protect your finances from the erosive impact of inflation.

In addition to the tips mentioned above, there are a few other strategies you can employ to shield yourself from inflation’s negative consequences. Negotiating your bills, shopping around for better deals, and utilizing credit cards with rewards programs can further help offset rising costs.

Remember, protecting yourself from inflation requires diligence and informed decision-making. By implementing these strategies, you can build a stronger financial foundation and maintain your purchasing power in the face of inflationary pressures.