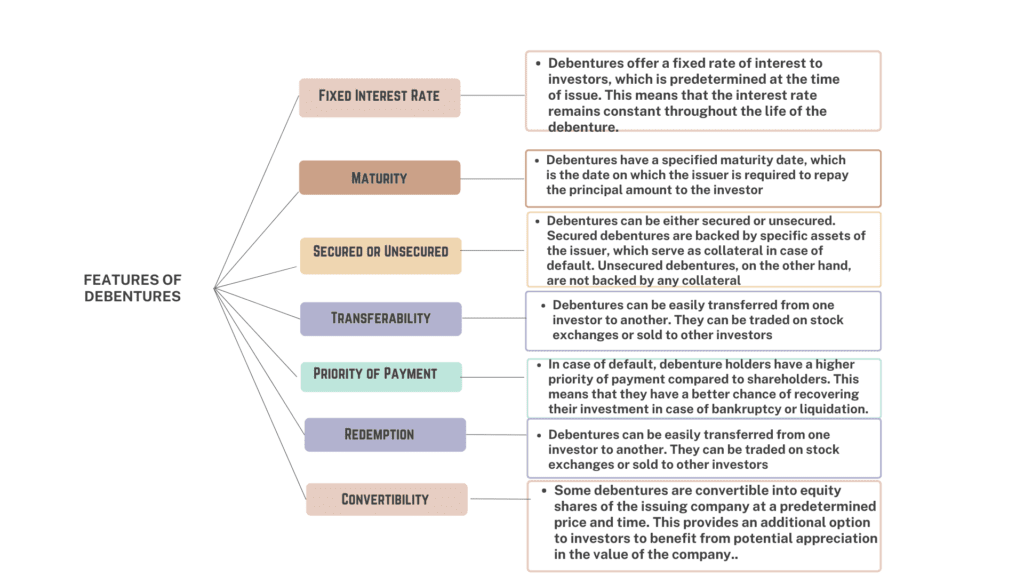

Debentures

A debenture is a type of bond that is not secured by any specific assets, but instead relies on the creditworthiness of the issuer. Debentures are typically issued by corporations or governments, and like bonds, pay the investor interest at regular intervals. Unlike bonds, however, debentures do not have any collateral backing them up, making them riskier investments. In the event of bankruptcy or default, debenture holders are treated as unsecured creditors and may not receive full repayment.

Advantages and Disadvantages of Issuing Debentures

Advantages

- Lower Cost of Capital: Debentures offer a lower cost of capital compared to equity financing because the interest paid on debentures is tax-deductible, while dividends paid to shareholders are not. This means that debenture financing is more cost-effective than equity financing.

- No Dilution of Ownership: Unlike equity financing, issuing debentures does not dilute the ownership of existing shareholders. The issuing organization retains full ownership and control over its operations.

- Flexible Repayment Options: Debentures can be issued with a variety of repayment options, including bullet payments, installment payments, and sinking fund payments. This provides flexibility to the issuing organization in managing its debt obligations.

- Diversification of Funding Sources: Issuing debentures allows organizations to diversify their sources of funding. By tapping into the debt market, organizations can reduce their reliance on bank loans and equity financing.

- Improve Creditworthiness: Issuing debentures can improve the creditworthiness of an organization. By demonstrating a track record of timely debt repayment, an organization can enhance its credit rating and gain access to cheaper sources of funding in the future.

- Long-term Financing: Debentures provide long-term financing, which is beneficial for capital-intensive projects that require significant upfront investment. This allows organizations to undertake large projects without putting undue pressure on their short-term cash flows.

Disadvantages

While debentures can offer several advantages to the issuing organization, there are also some disadvantages that need to be considered before issuing them. Some of the disadvantages of issuing debentures include:

- Interest and principal payments: The issuing organization is required to make regular interest payments and repay the principal amount on the maturity date, regardless of its financial performance. This can put a strain on the organization’s cash flow and limit its financial flexibility.

- Fixed obligations: Debentures represent a fixed obligation and must be repaid even if the issuing organization experiences financial difficulties or a downturn in its business operations. This can make it difficult for the organization to adapt to changing market conditions or investment opportunities.

- Credit risk: Debentures are a form of debt and represent a credit risk to the issuing organization. If the organization is unable to meet its debt obligations, it may default on the debentures, leading to a loss of investor confidence and potential legal action.

- Dilution of ownership: Issuing debentures may require the issuing organization to offer collateral or provide security, such as a lien on its assets. This can dilute the ownership rights of existing shareholders and reduce their share of profits and control over the organization.

- Cost of issuance: Issuing debentures involves various costs, such as legal fees, underwriting fees, and rating agency fees, which can add up and increase the overall cost of capital for the issuing organization.

Difference between Debentures and Bonds

| Characteristics | Bonds | Debentures |

| Owner | Bondholder | Debenture holder |

| Tenure | Typically 10 years or more, may have call/put options | Typically between 3 to 10 years, fixed maturity date without call/put options |

| Collateral | Secured by collateral or physical assets of issuing company | Not secured by collateral or physical assets |

| Security | Typically secured by specific assets or collateral | Unsecured and not backed by any specific assets |

| Priority | Higher priority for repayment than debenture holders in event of bankruptcy/default | Lower priority compared to bondholders and secured creditors |

| Interest rate | Lower interest rates due to security provided | Generally higher than bonds because they are unsecured |

| Convertibility | Some bonds are convertible into equity | Typically do not have this feature |

| Credit ratings | Issued by companies or governments with strong credit ratings | May be issued by companies with weaker credit ratings |

| Usage | Used to raise large amounts of capital for long-term projects | Used to raise smaller amounts of capital for shorter-term projects |

| Risk | Lower risk due to security provided | Generally considered riskier as they are unsecured |

| Terms | Often have more complex terms and conditions than debentures, with a greater variety of features | May include provisions for early redemption, conversion into equity, or other terms |

| Investor base | Often marketed to institutional investors such as pension funds, insurance companies, mutual funds, and hedge funds | May be marketed to retail investors |

| Denominations | Usually trade in larger denominations, making them less accessible to retail investors | Often trade in smaller denominations, making them more accessible to retail investors |

How to Issue Debentures

- Determine the terms of the debenture: The issuing organization must determine the terms of the debenture, including the interest rate, maturity date, and redemption options.

- Prepare a prospectus: The issuing organization must prepare a prospectus that provides detailed information about the debenture, including the terms and conditions, risks, and potential returns.

- Obtain necessary approvals: The issuing organization must obtain necessary approvals from regulatory authorities, such as the Securities and Exchange Commission (SEC) in the United States.

- Offer the debentures: The issuing organization can offer the debentures to the public through a public offering, or to select investors through a private placement.

- Allocate the debentures: The issuing organization must allocate the debentures to investors based on the terms of the offering.

- Issue the debentures: The issuing organization must issue the debentures to the investors and receive the proceeds from the offering.

- Service the debt: The issuing organization must service the debt by making regular interest payments and repaying the principal amount on the maturity date.

- Manage the debt: The issuing organization must manage the debt by monitoring its debt-to-equity ratio, maintaining adequate cash reserves, and managing interest rate risk.

Resources that can help you in investing in debentures.

You can also visit these websites that provide details about how to invest in debentures:

- Securities and Exchange Board of India (SEBI) – https://www.sebi.gov.in/

- National Stock Exchange (NSE) – https://www.nseindia.com/

- Bombay Stock Exchange (BSE) – https://www.bseindia.com/

- Reserve Bank of India (RBI) – https://www.rbi.org.in/

- India Infoline (IIFL) – https://www.indiainfoline.com/

- Angel Broking – https://www.angelbroking.com/

- Kotak Securities – https://www.kotaksecurities.com/

- HDFC Securities – https://www.hdfcsec.com/

- ICICI Direct – https://www.icicidirect.com/

- Zerodha – https://zerodha.com/

Conclusion

Debentures are an essential financial instrument used by companies to raise capital through loans from the public. There are different types of debentures that come with specific features and characteristics. Although debentures offer benefits like lower interest rates and flexibility, they also pose disadvantages like potential dilution of ownership and the risk of default. Ultimately, companies should make informed decisions on issuing debentures based on their specific needs and circumstances. Understanding the different types of debentures and their features can help make informed decisions on raising capital through this means.

Does credit rating of issuer company matter?

Please find out more information about this in our dedicated post on this subject.